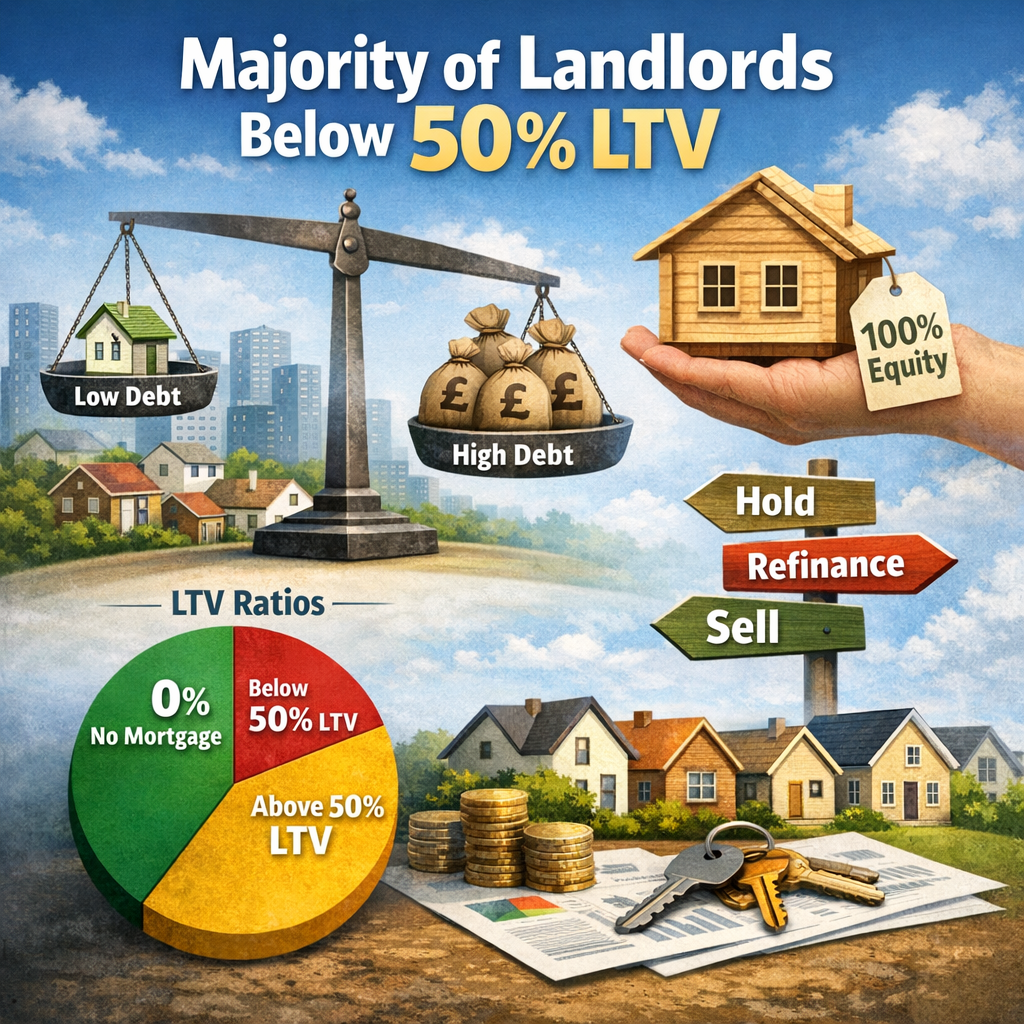

Most landlords now debt-light, with majority below 50% LTV

admin

admin

Property118

Most landlords now debt-light, with majority below 50% LTV

A widely held assumption about the private rented sector is that landlords are highly leveraged and therefore vulnerable to interest rate movements. The latest data suggests a different picture. According to the Property118 Landlord Sentiment Survey Q1 2026, most landlords are now operating with relatively low levels of borrowing.

Based on 2,380 completed responses, a majority of landlords report loan-to-value ratios at or below 50%, with a significant proportion owning properties outright with no mortgage debt at all. You can review the full dataset here.

The implication is clear: the sector is more resilient than it is often portrayed.

A different risk profile

At higher levels of borrowing, landlords are naturally more exposed to changes in interest rates and refinancing conditions. That exposure has shaped much of the public narrative over recent years. However, the survey findings point towards a different risk profile.

With many landlords holding significant equity and relatively modest debt, the immediate pressure from interest rate increases is less pronounced than often assumed. This does not remove risk entirely, but it changes its nature. The issue becomes less about survival and more about strategy.

Why this matters for market behaviour

The level of borrowing has a direct influence on how landlords respond to changing conditions. Highly leveraged landlords may be forced to act quickly when costs rise. By contrast, those with lower loan-to-value ratios have more flexibility. They can choose whether to refinance, hold, or sell, rather than being compelled into a decision.

This aligns with other findings from the Property118 dataset, which show that many landlords are planning to reduce portfolios despite not being under immediate financial pressure.

Equity creates options

Lower levels of borrowing mean higher levels of equity, and equity provides optionality.

Landlords with substantial equity can:

– sell selectively rather than under pressure

– refinance on more favourable terms

– release capital if required

– or simply hold assets without urgency

This flexibility changes the dynamics of the market. Rather than reacting to external pressures, many landlords are making proactive decisions about how their portfolios should evolve.

A shift in mindset

The combination of lower leverage and changing market conditions appears to be influencing how landlords think about their portfolios. For many, the focus is no longer on maximising growth through borrowing, but on consolidating gains, reducing complexity and improving long-term certainty. This is consistent with the broader trends highlighted in the survey results, including rising intentions to sell and a limited appetite for expansion.

A more stable, but more selective sector

A debt-light sector is, in many respects, a more stable one. Lower leverage reduces the risk of forced sales and financial distress. At the same time, it also means that landlords are under less pressure to remain active. When portfolios are secure and largely unencumbered, the decision to continue, expand or exit becomes a matter of choice rather than necessity.

For now, one conclusion stands out: landlords are not being pushed out by debt, they are choosing their next move from a position of strength.

A conversation worth having?

If you are weighing up your own strategy, whether that’s to sell, expand, or restructure to improve profitibility, it is worth having a discussion with a Property118 consultant to take a closer look at how your portfolio is structured as a whole now, and to forecast the outcomes based on multiple scenario’s.

These conversations are typically most useful for landlords with established portfolios and relatively modest borrowing who are beginning to reflect on how their assets could work more effectively in the years ahead.

/* “function”==typeof InitializeEditor,callIfLoaded:function(o){return!(!gform.domLoaded||!gform.scriptsLoaded||!gform.themeScriptsLoaded&&!gform.isFormEditor()||(gform.isFormEditor()&&console.warn(“The use of gform.initializeOnLoaded() is deprecated in the form editor context and will be removed in Gravity Forms 3.1.”),o(),0))},initializeOnLoaded:function(o){gform.callIfLoaded(o)||(document.addEventListener(“gform_main_scripts_loaded”,()=>{gform.scriptsLoaded=!0,gform.callIfLoaded(o)}),document.addEventListener(“gform/theme/scripts_loaded”,()=>{gform.themeScriptsLoaded=!0,gform.callIfLoaded(o)}),window.addEventListener(“DOMContentLoaded”,()=>{gform.domLoaded=!0,gform.callIfLoaded(o)}))},hooks:{action:{},filter:{}},addAction:function(o,r,e,t){gform.addHook(“action”,o,r,e,t)},addFilter:function(o,r,e,t){gform.addHook(“filter”,o,r,e,t)},doAction:function(o){gform.doHook(“action”,o,arguments)},applyFilters:function(o){return gform.doHook(“filter”,o,arguments)},removeAction:function(o,r){gform.removeHook(“action”,o,r)},removeFilter:function(o,r,e){gform.removeHook(“filter”,o,r,e)},addHook:function(o,r,e,t,n){null==gform.hooks[o][r]&&(gform.hooks[o][r]=[]);var d=gform.hooks[o][r];null==n&&(n=r+”_”+d.length),gform.hooks[o][r].push({tag:n,callable:e,priority:t=null==t?10:t})},doHook:function(r,o,e){var t;if(e=Array.prototype.slice.call(e,1),null!=gform.hooks[r][o]&&((o=gform.hooks[r][o]).sort(function(o,r){return o.priority-r.priority}),o.forEach(function(o){“function”!=typeof(t=o.callable)&&(t=window[t]),”action”==r?t.apply(null,e):e[0]=t.apply(null,e)})),”filter”==r)return e[0]},removeHook:function(o,r,t,n){var e;null!=gform.hooks[o][r]&&(e=(e=gform.hooks[o][r]).filter(function(o,r,e){return!!(null!=n&&n!=o.tag||null!=t&&t!=o.priority)}),gform.hooks[o][r]=e)}});

/* ]]> */

Enquire about a free initial discussion with a Property118 consultant

-

Mr.Mrs.MissMs.Dr.Prof.Rev.

-

-

Important Notice – Scope of Planning Support

Important Notice – Scope of Planning SupportWhere our recommendations touch on areas requiring regulated input, we refer clients to appropriately authorised professionals for advice and implementation.

-

-

-

/* = 0;if(!is_postback){return;}var form_content = jQuery(this).contents().find(‘#gform_wrapper_585′);var is_confirmation = jQuery(this).contents().find(‘#gform_confirmation_wrapper_585′).length > 0;var is_redirect = contents.indexOf(‘gformRedirect(){‘) >= 0;var is_form = form_content.length > 0 && ! is_redirect && ! is_confirmation;var mt = parseInt(jQuery(‘html’).css(‘margin-top’), 10) + parseInt(jQuery(‘body’).css(‘margin-top’), 10) + 100;if(is_form){jQuery(‘#gform_wrapper_585′).html(form_content.html());if(form_content.hasClass(‘gform_validation_error’)){jQuery(‘#gform_wrapper_585′).addClass(‘gform_validation_error’);} else {jQuery(‘#gform_wrapper_585′).removeClass(‘gform_validation_error’);}setTimeout( function() { /* delay the scroll by 50 milliseconds to fix a bug in chrome */ }, 50 );if(window[‘gformInitDatepicker’]) {gformInitDatepicker();}if(window[‘gformInitPriceFields’]) {gformInitPriceFields();}var current_page = jQuery(‘#gform_source_page_number_585′).val();gformInitSpinner( 585, ‘https://www.property118.com/wp-content/plugins/gravityforms/images/spinner.svg’, true );jQuery(document).trigger(‘gform_page_loaded’, [585, current_page]);window[‘gf_submitting_585′] = false;}else if(!is_redirect){var confirmation_content = jQuery(this).contents().find(‘.GF_AJAX_POSTBACK’).html();if(!confirmation_content){confirmation_content = contents;}jQuery(‘#gform_wrapper_585′).replaceWith(confirmation_content);jQuery(document).trigger(‘gform_confirmation_loaded’, [585]);window[‘gf_submitting_585′] = false;wp.a11y.speak(jQuery(‘#gform_confirmation_message_585′).text());}else{jQuery(‘#gform_585′).append(contents);if(window[‘gformRedirect’]) {gformRedirect();}}jQuery(document).trigger(“gform_pre_post_render”, [{ formId: “585”, currentPage: “current_page”, abort: function() { this.preventDefault(); } }]); if (event && event.defaultPrevented) { return; } const gformWrapperDiv = document.getElementById( “gform_wrapper_585″ ); if ( gformWrapperDiv ) { const visibilitySpan = document.createElement( “span” ); visibilitySpan.id = “gform_visibility_test_585″; gformWrapperDiv.insertAdjacentElement( “afterend”, visibilitySpan ); } const visibilityTestDiv = document.getElementById( “gform_visibility_test_585″ ); let postRenderFired = false; function triggerPostRender() { if ( postRenderFired ) { return; } postRenderFired = true; gform.core.triggerPostRenderEvents( 585, current_page ); if ( visibilityTestDiv ) { visibilityTestDiv.parentNode.removeChild( visibilityTestDiv ); } } function debounce( func, wait, immediate ) { var timeout; return function() { var context = this, args = arguments; var later = function() { timeout = null; if ( !immediate ) func.apply( context, args ); }; var callNow = immediate && !timeout; clearTimeout( timeout ); timeout = setTimeout( later, wait ); if ( callNow ) func.apply( context, args ); }; } const debouncedTriggerPostRender = debounce( function() { triggerPostRender(); }, 200 ); if ( visibilityTestDiv && visibilityTestDiv.offsetParent === null ) { const observer = new MutationObserver( ( mutations ) => { mutations.forEach( ( mutation ) => { if ( mutation.type === ‘attributes’ && visibilityTestDiv.offsetParent !== null ) { debouncedTriggerPostRender(); observer.disconnect(); } }); }); observer.observe( document.body, { attributes: true, childList: false, subtree: true, attributeFilter: [ ‘style’, ‘class’ ], }); } else { triggerPostRender(); } } );} );

/* ]]> */

|

★★★★★

|

Help other landlords find Property118If you have found Property118 useful, a short Trustpilot review would make a meaningful difference. It helps other landlords decide whether our research is worth following. |

The post Most landlords now debt-light, with majority below 50% LTV appeared first on Property118.

View Full Article: Most landlords now debt-light, with majority below 50% LTV

Mayor of London urged to take action as key workers struggle with rent

Property118

Mayor of London urged to take action as key workers struggle with rent

Renting in London is now unaffordable for key workers, as a tenant group urges the Mayor of London to do more to tackle soaring rents.

Research by Generation Rent reveals teachers, nurses and bus drivers would struggle to rent the average one-bed home in most London boroughs.

Generation Rent is calling on London Mayor Sadiq Khan to “slam the brakes on local rents for key workers”.

Nine types of key workers would fail letting agent affordability checks

According to Generation Rent, nine types of key workers would fail letting agent affordability checks for the average one-bed home in every London borough, with average London wages worth less than 2.5 times the average rent.

In seven boroughs, the average one-bed home demands more rent than the average hairdresser in London earns in a year, with the rent in Kensington and Chelsea worth 138% of a hairdresser’s income of £22,641.

Across Greater London, the average monthly rent of £1,688 consumes. 40% of a community nurse’s income, 71% of a receptionist’s income, 80% of a pharmacy assistant’s income and 79% of a teaching assistant’s income

The most expensive borough was Kensington and Chelsea with the average rent for a 1-bed of £2,595 per month, and the cheapest was Bexley, with £1,138.

Slam the brakes on local rents

Dan Wilson Craw, deputy chief executive of Generation Rent, said: “London is one of the richest cities on the planet, but it depends on the key workers who clean up after us, take care of our sick and elderly, and drive our buses to where we need to go.

“London needs its key workers if the city can continue to thrive, but those workers cannot stay in a city that demands an arm and a leg for a place to recharge after a hard day and build their life from.

“The current cost of the renting crisis is devastating for London’s essential occupations and the rest of us. It is vital that the Mayor is given the power to slam the brakes on local rents and give our key workers the breathing space they need to live and work in their community. It is also vital that the mayor and the government build more affordable homes in the capital and increase how much social housing is available.”

As previously reported by Property118, London Mayor Sadiq Khan has pushed for rent controls under new devolution powers.

Mr Khan admitted that, in his conversations with the Labour government, ministers had been “not keen” on rent controls but said he would keep trying.

The post Mayor of London urged to take action as key workers struggle with rent appeared first on Property118.

View Full Article: Mayor of London urged to take action as key workers struggle with rent

Tenants told how to challenge rent repayment orders

Property118

Tenants told how to challenge rent repayment orders

The government has released guidance for tenants on challenging landlords through rent repayment orders.

Under the Renters’ Rights Act, landlords face tougher penalties, with the maximum amount of rent they can be ordered to repay doubling from 12 to 24 months.

The government has also published separate guidance for tenants on the court eviction process under the Act.

Tenants can prove an offence has been committed

The government says the guidance is “primarily intended for tenants in the private rented sector, but councils may also find it useful when applying for Rent Repayment Orders.”

The government guidance explains that tenants can challenge their landlord by proving an offence has been committed, such as operating an unlicensed HMO or failing to obtain a selective licence.

According to the government guidance, tenants can check whether a landlord has committed an offence by:

- Typing the name of their council followed by “landlord licensing scheme” into a search engine to find details of any schemes in place.

- Searching for the council’s “landlord licensing register”. The guidance notes that some councils publish a public register of licensed properties, while others do not. If a property does not appear, this does not necessarily mean it is unlicensed, as registers may not always be up to date.

- Contacting the council directly if the property cannot be found on the register.

The government guidance advises tenants to also include the address, the dates they lived at the property and the number of unrelated people they shared the home with

It also says tenants should ask the council:

- whether the property is licensable

- if so, whether it currently holds a licence under any local scheme

- whether a valid licence application or Temporary Exemption Notice (TEN) has been submitted

- and, if applicable, the effective date of that application or TEN

Selective licence offence

The government guidance says that to prove a landlord has committed an offence by failing to hold a selective licence, tenants must show:

- the council had a selective licensing scheme covering the property

- the property was privately rented

- the landlord did not hold a licence

It explains that tenants should include evidence in their application bundle such as:

- a copy of the council’s licensing scheme and confirmation it covered their postcode

- proof the property was privately rented, including witness statements, tenancy agreements and deposit documents

- confirmation from the council that the property was not licensed

The guidance also advises including supporting material such as communications with the landlord or letting agent.

Elsewhere in the guidance, it gives a list of the defences landlords may use such as reasonable excuse. The guidance says: “To argue this successfully, the First Tier Tribunal needs to be satisfied that the landlord has a valid reason for not meeting the legal requirement.”

Severe consequences for landlords

As previously reported by Property118, Landlord Licensing & Defence expert Des Taylor warns rent repayment orders are a serious offence with potentially severe consequences for landlords.

He said: “Rent repayment orders are strict liability offences. If a property was unlicensed when the law required one, the landlord is guilty regardless of whether the agent failed them or they were unaware of the requirement.”

The only defence, Mr Taylor says, is to have the evidence that proves the landlord’s case.

This means time-stamped proof of a licence application, payment receipts, bank statements, council acknowledgements and detailed phone call records. Without this, the tribunal will take the council’s word that no valid licence existed.

The post Tenants told how to challenge rent repayment orders appeared first on Property118.

View Full Article: Tenants told how to challenge rent repayment orders

RICS survey shows housing slowdown and rising rents

Property118

RICS survey shows housing slowdown and rising rents

Tenant demand rose again in March even as the housing market lost momentum, the Royal Institution of Chartered Surveyors (RICS) says.

Its member survey for March shows that lettings demand edged up to 10%, but landlord instructions stayed at -25%.

Members are also highlighting that rents will continue rising over the short term.

Buyer enquiries fall

The monthly survey also shows that new home buyer enquiries fell to a net balance of -39%, from -29% in February, in the weakest reading since August 2023.

It adds that the weaker sales activity is down to rising borrowing costs and Middle East tensions.

Agreed sales, meanwhile, dropped to -34% from -13% a month earlier.

Short-term sales expectations fell sharply to -33%, compared with -4% in February.

House prices to soften

The 12-month outlook also slipped to -1%, losing the modest positive position seen previously.

Prices showed further softening through March as the headline price balance came in at -23%, down from -14% and -10% in the two months before.

Expectations over the next three months weakened to -43%, while the 12-month view edged to +2%.

Across the regions, London, East Anglia, the South East and the South West all recorded readings below the national average.

Scotland and Northern Ireland continued to report positive price balances.

New instructions remained subdued at -6%, and unsold stock rose to an average of 47 properties, up from roughly 45 at the start of the year.

Conflict brings housing market issues

Tarrant Parsons, RICS’ head of market research and analysis, said: “The mood across the UK housing market has shifted markedly over the past couple of months.

“What had been a cautiously improving picture for activity has been knocked off course by the wider macro fallout from the Middle East conflict, as the renewed deterioration in the mortgage rate outlook has proved particularly challenging.”

He added: “Indeed, with average fixed rates climbing back above 5% according to some sources, it is unsurprising that buyer demand has softened.

“The path ahead hinges on whether or not recent surges in oil and energy costs begin to reverse in what remains a highly uncertain geopolitical environment.”

Tom Bill, the head of UK residential research at Knight Frank, said: “Sentiment in the UK housing market will improve if the two-week ceasefire in the Middle East holds, supporting transaction levels as the spring market gets underway.

“However, mortgage rates won’t snap back to where they were in February due to the longer-term inflationary impact of the war and the associated vulnerability of the government’s financial position, which will keep house prices in check.”

The post RICS survey shows housing slowdown and rising rents appeared first on Property118.

View Full Article: RICS survey shows housing slowdown and rising rents

UK rental market dominated by landlords aged over 55

Property118

UK rental market dominated by landlords aged over 55

A striking demographic pattern has emerged from the latest UK landlord data, and it raises important questions about the future of the private rented sector. According to the Property118 Landlord Sentiment Survey Q1 2026, the overwhelming majority of landlords are now aged 56 and above, with very limited representation from younger investors.

Based on 2,380 completed responses, 76.8% of landlords fall into the 56+ age bracket, while fewer than 3% are under the age of 40. You can explore the full survey findings here.

The implication is immediate: the UK rental market is increasingly reliant on an ageing landlord base.

A generational imbalance

At a glance, the data highlights a widening gap between those currently operating in the sector and those entering it. Older landlords dominate the landscape, while younger participation remains extremely limited. This is not simply a reflection of experience or time in the market, it points towards a deeper structural issue: fewer new entrants mean fewer replacements.

As existing landlords begin to reduce portfolios or exit entirely, the absence of a younger pipeline becomes more significant.

Barriers to entry are becoming more visible

The survey results do not explicitly ask why younger landlords are underrepresented, but the broader context offers some clues. Higher entry costs, tighter lending criteria and increased regulatory complexity all contribute to a more challenging environment for new investors. In addition, the shift in tax treatment over recent years has made it more difficult for individuals to build portfolios in the same way previous generations did. The result is a market that is not naturally replenishing itself.

Experience concentrated at the top end

The age profile of landlords also aligns with the size and maturity of their portfolios.

As highlighted in the Property118 dataset, the average respondent owns 9.7 rental properties, suggesting that much of the sector is controlled by experienced, long-term investors. This concentration of experience brings stability, but it also introduces a dependency. When a large proportion of housing supply is managed by landlords approaching or already in later life, future supply becomes increasingly tied to their personal decisions.

What happens next?

The demographic imbalance would be less significant if younger landlords were entering the market at a similar pace, but the survey data suggests that this is not currently the case. At the same time, as explored in the wider survey findings, a meaningful proportion of existing landlords are already considering reducing their portfolios or exiting altogether. This creates a simple but important question; if older landlords begin to step back, who replaces them?

A structural issue in the making

Demographic trends tend to move slowly, but their impact can be long-lasting.

An ageing landlord base, combined with limited new entrants, points towards a gradual tightening of supply over time, particularly if exit intentions translate into completed sales.

This is not an immediate shock to the system, but it is a clear directional signal.

For now, one conclusion stands out: the future of the rental market is increasingly shaped by landlords nearing the end of their investment journey, not those just beginning it.

A conversation worth having?

If you are weighing up your own strategy, whether that’s to sell, expand, or restructure to improve profitibility, it is worth having a discussion with a Property118 consultant to take a closer look at how your portfolio is structured as a whole now, and to forecast the outcomes based on multiple scenario’s.

These conversations are typically most useful for landlords with established portfolios and relatively modest borrowing who are beginning to reflect on how their assets could work more effectively in the years ahead.

/* “function”==typeof InitializeEditor,callIfLoaded:function(o){return!(!gform.domLoaded||!gform.scriptsLoaded||!gform.themeScriptsLoaded&&!gform.isFormEditor()||(gform.isFormEditor()&&console.warn(“The use of gform.initializeOnLoaded() is deprecated in the form editor context and will be removed in Gravity Forms 3.1.”),o(),0))},initializeOnLoaded:function(o){gform.callIfLoaded(o)||(document.addEventListener(“gform_main_scripts_loaded”,()=>{gform.scriptsLoaded=!0,gform.callIfLoaded(o)}),document.addEventListener(“gform/theme/scripts_loaded”,()=>{gform.themeScriptsLoaded=!0,gform.callIfLoaded(o)}),window.addEventListener(“DOMContentLoaded”,()=>{gform.domLoaded=!0,gform.callIfLoaded(o)}))},hooks:{action:{},filter:{}},addAction:function(o,r,e,t){gform.addHook(“action”,o,r,e,t)},addFilter:function(o,r,e,t){gform.addHook(“filter”,o,r,e,t)},doAction:function(o){gform.doHook(“action”,o,arguments)},applyFilters:function(o){return gform.doHook(“filter”,o,arguments)},removeAction:function(o,r){gform.removeHook(“action”,o,r)},removeFilter:function(o,r,e){gform.removeHook(“filter”,o,r,e)},addHook:function(o,r,e,t,n){null==gform.hooks[o][r]&&(gform.hooks[o][r]=[]);var d=gform.hooks[o][r];null==n&&(n=r+”_”+d.length),gform.hooks[o][r].push({tag:n,callable:e,priority:t=null==t?10:t})},doHook:function(r,o,e){var t;if(e=Array.prototype.slice.call(e,1),null!=gform.hooks[r][o]&&((o=gform.hooks[r][o]).sort(function(o,r){return o.priority-r.priority}),o.forEach(function(o){“function”!=typeof(t=o.callable)&&(t=window[t]),”action”==r?t.apply(null,e):e[0]=t.apply(null,e)})),”filter”==r)return e[0]},removeHook:function(o,r,t,n){var e;null!=gform.hooks[o][r]&&(e=(e=gform.hooks[o][r]).filter(function(o,r,e){return!!(null!=n&&n!=o.tag||null!=t&&t!=o.priority)}),gform.hooks[o][r]=e)}});

/* ]]> */

Enquire about a free initial discussion with a Property118 consultant

-

Mr.Mrs.MissMs.Dr.Prof.Rev.

-

-

Important Notice – Scope of Planning Support

Where our recommendations touch on areas requiring regulated input, we refer clients to appropriately authorised professionals for advice and implementation.

-

-

-

/* = 0;if(!is_postback){return;}var form_content = jQuery(this).contents().find(‘#gform_wrapper_585′);var is_confirmation = jQuery(this).contents().find(‘#gform_confirmation_wrapper_585′).length > 0;var is_redirect = contents.indexOf(‘gformRedirect(){‘) >= 0;var is_form = form_content.length > 0 && ! is_redirect && ! is_confirmation;var mt = parseInt(jQuery(‘html’).css(‘margin-top’), 10) + parseInt(jQuery(‘body’).css(‘margin-top’), 10) + 100;if(is_form){jQuery(‘#gform_wrapper_585′).html(form_content.html());if(form_content.hasClass(‘gform_validation_error’)){jQuery(‘#gform_wrapper_585′).addClass(‘gform_validation_error’);} else {jQuery(‘#gform_wrapper_585′).removeClass(‘gform_validation_error’);}setTimeout( function() { /* delay the scroll by 50 milliseconds to fix a bug in chrome */ }, 50 );if(window[‘gformInitDatepicker’]) {gformInitDatepicker();}if(window[‘gformInitPriceFields’]) {gformInitPriceFields();}var current_page = jQuery(‘#gform_source_page_number_585′).val();gformInitSpinner( 585, ‘https://www.property118.com/wp-content/plugins/gravityforms/images/spinner.svg’, true );jQuery(document).trigger(‘gform_page_loaded’, [585, current_page]);window[‘gf_submitting_585′] = false;}else if(!is_redirect){var confirmation_content = jQuery(this).contents().find(‘.GF_AJAX_POSTBACK’).html();if(!confirmation_content){confirmation_content = contents;}jQuery(‘#gform_wrapper_585′).replaceWith(confirmation_content);jQuery(document).trigger(‘gform_confirmation_loaded’, [585]);window[‘gf_submitting_585′] = false;wp.a11y.speak(jQuery(‘#gform_confirmation_message_585′).text());}else{jQuery(‘#gform_585′).append(contents);if(window[‘gformRedirect’]) {gformRedirect();}}jQuery(document).trigger(“gform_pre_post_render”, [{ formId: “585”, currentPage: “current_page”, abort: function() { this.preventDefault(); } }]); if (event && event.defaultPrevented) { return; } const gformWrapperDiv = document.getElementById( “gform_wrapper_585″ ); if ( gformWrapperDiv ) { const visibilitySpan = document.createElement( “span” ); visibilitySpan.id = “gform_visibility_test_585″; gformWrapperDiv.insertAdjacentElement( “afterend”, visibilitySpan ); } const visibilityTestDiv = document.getElementById( “gform_visibility_test_585″ ); let postRenderFired = false; function triggerPostRender() { if ( postRenderFired ) { return; } postRenderFired = true; gform.core.triggerPostRenderEvents( 585, current_page ); if ( visibilityTestDiv ) { visibilityTestDiv.parentNode.removeChild( visibilityTestDiv ); } } function debounce( func, wait, immediate ) { var timeout; return function() { var context = this, args = arguments; var later = function() { timeout = null; if ( !immediate ) func.apply( context, args ); }; var callNow = immediate && !timeout; clearTimeout( timeout ); timeout = setTimeout( later, wait ); if ( callNow ) func.apply( context, args ); }; } const debouncedTriggerPostRender = debounce( function() { triggerPostRender(); }, 200 ); if ( visibilityTestDiv && visibilityTestDiv.offsetParent === null ) { const observer = new MutationObserver( ( mutations ) => { mutations.forEach( ( mutation ) => { if ( mutation.type === ‘attributes’ && visibilityTestDiv.offsetParent !== null ) { debouncedTriggerPostRender(); observer.disconnect(); } }); }); observer.observe( document.body, { attributes: true, childList: false, subtree: true, attributeFilter: [ ‘style’, ‘class’ ], }); } else { triggerPostRender(); } } );} );

/* ]]> */

|

★★★★★

|

Help other landlords find Property118If you have found Property118 useful, a short Trustpilot review would make a meaningful difference. It helps other landlords decide whether our research is worth following. |

The post UK rental market dominated by landlords aged over 55 appeared first on Property118.

View Full Article: UK rental market dominated by landlords aged over 55

Firm warns of council bureaucracy as landlord fined £5,000 over minor mistake

Property118

Firm warns of council bureaucracy as landlord fined £5,000 over minor mistake

A legal expert has accused councils of using “bureaucracy as a weapon to generate enforcement revenue” after a landlord was fined £5,000 for ticking the wrong box on a Houses in Multiple Occupation (HMO) form.

Phil Turtle from Landlord Licensing & Defence is warning landlords that minor application errors could cost them thousands of pounds in fines.

The firm helped one landlord after a council in the Midlands penalised them for inadvertently ticking the wrong box on HMO application forms.

The landlord only became exposed to enforcement because the council chose to refund their licence fee on the basis that they had applied for the wrong type of HMO licence.

Unregulated, unaccountable and landlord-hating

Landlord Licensing & Defence warns other councils are rejecting HMO applications where a landlord inadvertently uses an ‘additional’ licensing form instead of a ‘mandatory’ form, or vice versa.

Even though the schemes require the same physical licences and identical conditions.

The firm explains by rejecting the application and refunding the fee, which is often done without notifying the landlord, the council effectively removes the landlord’s statutory protection of having an ‘application duly made’ under the Housing Act 2004.

Once that protection is gone, councils are promptly issuing Civil Penalty Fines for the operation of an unlicensed HMO.

Phil Turtle, the compliance director at Landlord Licensing & Defence, said: “Whilst we achieved a reduction in this case, the council refused to accept they had created the situation.

“They have no right in law to refuse an HMO licence application simply because it was the ‘wrong sort’ of HMO application, but they are unregulated, unaccountable and frankly, landlord-hating.

“It is the classic equivalent of British Rail blaming ‘the wrong sort of snow’ on the line!”

He continued: “Sadly, the landlord was not prepared to take this to the First-tier Tribunal because of the severe reputational damage that a public airing would inflict on their business, which would have carried a far greater impact than the fine itself.

“Effectively, a landlord was bullied into accepting the council’s unlawful action as their own guilt!”

Councils are acting unlawfully

Mr Turtle adds that under the Housing Act 2004, there is no legal justification for a local authority to refuse or refund an HMO licence application that has otherwise been duly made just because the landlord did not understand the difference between two identical schemes or ticked the wrong box.

He said: “It’s obviously morally repugnant. The licences for most councils are exactly the same and rarely state whether they are mandatory or additional on the final document.

“By acting in this manner, councils are acting unlawfully and, as will surprise no-one, immorally. They are using pure bureaucracy as a weapon to generate enforcement revenue rather than to improve housing standards.”

Landlord Licensing & Defence are urging landlords to check their local council’s licensing criteria or seek professional representation when submitting HMO applications to avoid falling victim to these traps.

Landlords can book a no-charge, no-commitment 10-minute diagnostic call with an expert on HMO and selective licensing or other compliance matters by clicking here or by calling 0208 088 8393.

The post Firm warns of council bureaucracy as landlord fined £5,000 over minor mistake appeared first on Property118.

View Full Article: Firm warns of council bureaucracy as landlord fined £5,000 over minor mistake

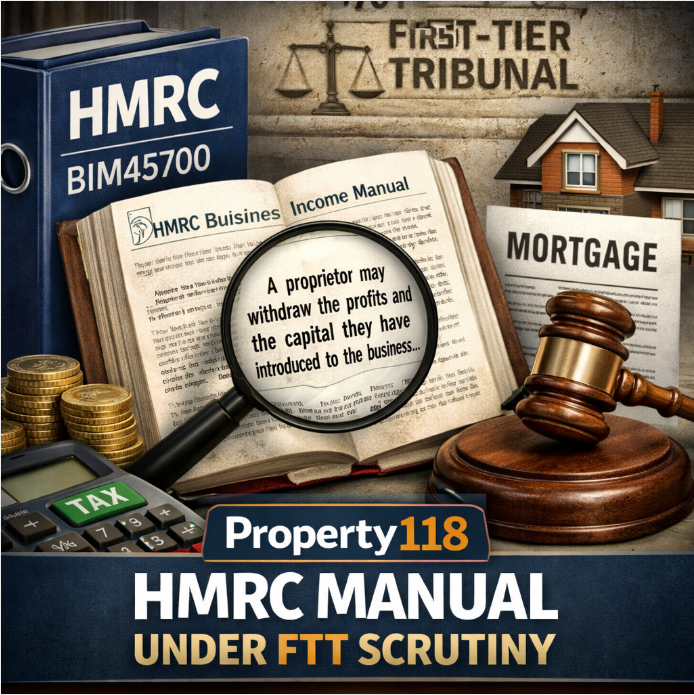

Property118 puts HMRC manual BIM45700 under FTT scrutiny

Property118

Property118 puts HMRC manual BIM45700 under FTT scrutiny

Since late 2023, HMRC has argued that financing the withdrawal of a positive capital account balance prior to incorporation of a business is a notifiable tax avoidance scheme under DOTAS legislation.

From our perspective, this makes no sense because that practice is supported by highly regarded industry textbook guidance published by Lexis Nexis, which says as follows …

Simon’s Taxes B9:114 – refinancing and ESC D32 considerations

If there is a substantial capital account in the unincorporated business, the business owner(s) should be advised to draw this down before incorporation, otherwise that capital will be locked into the value of the shares.

More importantly, HMRC’s own manual BIM45700 clearly states:

A proprietor of a business may withdraw the profits of the business and the capital they have introduced to the business, even though substitute funding then has to be provided by interest bearing loans. The interest payable on the loans is an allowable deduction. This is on the basis that the purpose of the additional borrowing is to provide working capital for the business. There will, though, be an interest restriction if the proprietor’s capital account becomes overdrawn, see BIM45705 onwards.

Source: https://www.gov.uk/hmrc-internal-manuals/business-income-manual/bim45700

HMRC has also recently taken the currently unpublished view (discovered via an FOI request) that if a company takes on new mortgages and uses those funds to redeem existing pre-incorporation mortgage liabilities, such funds could be treated as taxable consideration under CGT rules.

Important context: Property118 is not currently recommending Section 162 incorporation for landlords with mortgages while legal uncertainty remains over the treatment of mortgage liabilities. Read our current position here: Why Property118 is not currently recommending s162 incorporation to landlords with mortgages

The reason for our current position is not that the underlying principles are wrong, but that HMRC’s current interpretation conflicts with its own published guidance.

The above is intended to serve as a warning not only to landlords, but also to accountants, solicitors, barristers, mortgage brokers, lenders and financial advisers.

What our critics say

Some influencers have suggested that the timing of the financing of capital withdrawn, being so close to the date of incorporation, is abusive. We disagree on the basis that there is no evidence supported by legislation or HMRC manuals to support this stance, hence taking the case to the FTT.

They also argue that using the funds to loan to the company, immediately post-incorporation, and for the company to repay the debt quickly, is also abusive. Again, we disagree based on the same principles.

Finally, our critics have suggested that transferring only beneficial interest at incorporation is also abusive and constitutes a breach of mortgage terms, and that mortgage novation is the only acceptable method. Again, we disagree on the basis that it is common knowledge that taxation follows beneficial interest and that the Law of Property Act 1925 protects the interests of mortgage lenders even if liabilities are indemnified without the lender’s consent or knowledge. Furthermore, novation has not been mentioned in the relevant HMRC manuals since the phrase indemnity was introduced into them over 50 years ago, and in any event, very few, if any, mortgage lenders now offer novation.

Tribunal outcome

We expect the First-tier tribunal to make a ruling later this year, but the losing side could then appeal to the Upper Tribunal and beyond, resulting in the wait for much need clarity potentially being pushed back even further. Meanwhile, these matters continue to frustrate landlords who would like to incorporate their businesses for the reasons explained in HMRC’s GAAR Guidance Part D paragraph 2.2, as follows …

GAAR guidance – D2.2 intended legislative choice

D2.2

D2.2.1 This covers, for example, giving assets to children to reduce future Inheritance Tax liabilities, sacrificing salary in return for enhanced pension rights, disclaiming capital allowances to preserve reliefs for a later period, deciding to incorporate a business or to sell shares rather than assets (in both cases so as to pay less tax or Stamp Duty Land Tax) and choosing to borrow to invest in buy to let rather than using surplus cash or having a bigger mortgage on your main residence.

D2.2.2 These are all clearly things that are recognised by the statute: Parliament has given taxpayers a choice as to the course of action to take. This category might also include reorganising a trust or corporate structure in a straightforward way to fit in with a new tax regime.

The commercial reasons landlords choose to incorporate their rental property business were also documented in a report published by the Office of Tax Simplification in November 2022.

Source: https://www.gov.uk/government/publications/ots-review-of-residential-property-income

A conversation worth having?

If you are weighing up your own strategy, whether that’s to sell, expand, or restructure to improve profitability, it is worth having a discussion with a Property118 consultant to take a closer look at how your portfolio is structured as a whole now, and to forecast the outcomes based on multiple scenarios.

These conversations are typically most useful for landlords with established portfolios and relatively modest borrowing who are beginning to reflect on how their assets could work more effectively in the years ahead.

/* “function”==typeof InitializeEditor,callIfLoaded:function(o){return!(!gform.domLoaded||!gform.scriptsLoaded||!gform.themeScriptsLoaded&&!gform.isFormEditor()||(gform.isFormEditor()&&console.warn(“The use of gform.initializeOnLoaded() is deprecated in the form editor context and will be removed in Gravity Forms 3.1.”),o(),0))},initializeOnLoaded:function(o){gform.callIfLoaded(o)||(document.addEventListener(“gform_main_scripts_loaded”,()=>{gform.scriptsLoaded=!0,gform.callIfLoaded(o)}),document.addEventListener(“gform/theme/scripts_loaded”,()=>{gform.themeScriptsLoaded=!0,gform.callIfLoaded(o)}),window.addEventListener(“DOMContentLoaded”,()=>{gform.domLoaded=!0,gform.callIfLoaded(o)}))},hooks:{action:{},filter:{}},addAction:function(o,r,e,t){gform.addHook(“action”,o,r,e,t)},addFilter:function(o,r,e,t){gform.addHook(“filter”,o,r,e,t)},doAction:function(o){gform.doHook(“action”,o,arguments)},applyFilters:function(o){return gform.doHook(“filter”,o,arguments)},removeAction:function(o,r){gform.removeHook(“action”,o,r)},removeFilter:function(o,r,e){gform.removeHook(“filter”,o,r,e)},addHook:function(o,r,e,t,n){null==gform.hooks[o][r]&&(gform.hooks[o][r]=[]);var d=gform.hooks[o][r];null==n&&(n=r+”_”+d.length),gform.hooks[o][r].push({tag:n,callable:e,priority:t=null==t?10:t})},doHook:function(r,o,e){var t;if(e=Array.prototype.slice.call(e,1),null!=gform.hooks[r][o]&&((o=gform.hooks[r][o]).sort(function(o,r){return o.priority-r.priority}),o.forEach(function(o){“function”!=typeof(t=o.callable)&&(t=window[t]),”action”==r?t.apply(null,e):e[0]=t.apply(null,e)})),”filter”==r)return e[0]},removeHook:function(o,r,t,n){var e;null!=gform.hooks[o][r]&&(e=(e=gform.hooks[o][r]).filter(function(o,r,e){return!!(null!=n&&n!=o.tag||null!=t&&t!=o.priority)}),gform.hooks[o][r]=e)}});

/* ]]> */

Enquire about a free initial discussion with a Property118 consultant

-

Mr.Mrs.MissMs.Dr.Prof.Rev.

-

-

Important Notice – Scope of Planning Support

Where our recommendations touch on areas requiring regulated input, we refer clients to appropriately authorised professionals for advice and implementation.

-

-

-

/* = 0;if(!is_postback){return;}var form_content = jQuery(this).contents().find(‘#gform_wrapper_585′);var is_confirmation = jQuery(this).contents().find(‘#gform_confirmation_wrapper_585′).length > 0;var is_redirect = contents.indexOf(‘gformRedirect(){‘) >= 0;var is_form = form_content.length > 0 && ! is_redirect && ! is_confirmation;var mt = parseInt(jQuery(‘html’).css(‘margin-top’), 10) + parseInt(jQuery(‘body’).css(‘margin-top’), 10) + 100;if(is_form){jQuery(‘#gform_wrapper_585′).html(form_content.html());if(form_content.hasClass(‘gform_validation_error’)){jQuery(‘#gform_wrapper_585′).addClass(‘gform_validation_error’);} else {jQuery(‘#gform_wrapper_585′).removeClass(‘gform_validation_error’);}setTimeout( function() { /* delay the scroll by 50 milliseconds to fix a bug in chrome */ }, 50 );if(window[‘gformInitDatepicker’]) {gformInitDatepicker();}if(window[‘gformInitPriceFields’]) {gformInitPriceFields();}var current_page = jQuery(‘#gform_source_page_number_585′).val();gformInitSpinner( 585, ‘https://www.property118.com/wp-content/plugins/gravityforms/images/spinner.svg’, true );jQuery(document).trigger(‘gform_page_loaded’, [585, current_page]);window[‘gf_submitting_585′] = false;}else if(!is_redirect){var confirmation_content = jQuery(this).contents().find(‘.GF_AJAX_POSTBACK’).html();if(!confirmation_content){confirmation_content = contents;}jQuery(‘#gform_wrapper_585′).replaceWith(confirmation_content);jQuery(document).trigger(‘gform_confirmation_loaded’, [585]);window[‘gf_submitting_585′] = false;wp.a11y.speak(jQuery(‘#gform_confirmation_message_585′).text());}else{jQuery(‘#gform_585′).append(contents);if(window[‘gformRedirect’]) {gformRedirect();}}jQuery(document).trigger(“gform_pre_post_render”, [{ formId: “585”, currentPage: “current_page”, abort: function() { this.preventDefault(); } }]); if (event && event.defaultPrevented) { return; } const gformWrapperDiv = document.getElementById( “gform_wrapper_585″ ); if ( gformWrapperDiv ) { const visibilitySpan = document.createElement( “span” ); visibilitySpan.id = “gform_visibility_test_585″; gformWrapperDiv.insertAdjacentElement( “afterend”, visibilitySpan ); } const visibilityTestDiv = document.getElementById( “gform_visibility_test_585″ ); let postRenderFired = false; function triggerPostRender() { if ( postRenderFired ) { return; } postRenderFired = true; gform.core.triggerPostRenderEvents( 585, current_page ); if ( visibilityTestDiv ) { visibilityTestDiv.parentNode.removeChild( visibilityTestDiv ); } } function debounce( func, wait, immediate ) { var timeout; return function() { var context = this, args = arguments; var later = function() { timeout = null; if ( !immediate ) func.apply( context, args ); }; var callNow = immediate && !timeout; clearTimeout( timeout ); timeout = setTimeout( later, wait ); if ( callNow ) func.apply( context, args ); }; } const debouncedTriggerPostRender = debounce( function() { triggerPostRender(); }, 200 ); if ( visibilityTestDiv && visibilityTestDiv.offsetParent === null ) { const observer = new MutationObserver( ( mutations ) => { mutations.forEach( ( mutation ) => { if ( mutation.type === ‘attributes’ && visibilityTestDiv.offsetParent !== null ) { debouncedTriggerPostRender(); observer.disconnect(); } }); }); observer.observe( document.body, { attributes: true, childList: false, subtree: true, attributeFilter: [ ‘style’, ‘class’ ], }); } else { triggerPostRender(); } } );} );

/* ]]> */

|

★★★★★

|

Help other landlords find Property118If you have found Property118 useful, a short Trustpilot review would make a meaningful difference. It helps other landlords decide whether our research is worth following. |

The post Property118 puts HMRC manual BIM45700 under FTT scrutiny appeared first on Property118.

View Full Article: Property118 puts HMRC manual BIM45700 under FTT scrutiny

House prices dip in March as annual growth also slows

Property118

House prices dip in March as annual growth also slows

House prices fell by 0.5% last month, reversing a 0.3% rise in February and leaving the average property value at £299,677, Halifax reveals.

Its data also shows that annual growth slowed down to 0.8%, down from 1.2% in March.

Regional house price differences remain and these are more pronounced, with stronger gains recorded outside southern markets.

Northern Ireland continues to record the strongest annual house price growth, with average values up 8.7% to £224,809.

Scotland also posted an increase of 4.4%, taking the average property price to £222,716.

Regional house prices

Wales saw prices rise by 1.6% over the year, with the typical home now valued at £230,909.

Across England, higher growth remains concentrated in northern regions.

The North East recorded a 5% annual increase, with prices at £184,119, while the North West saw values rise 3.1% to an average of £247,442.

In southern markets, prices moved lower and the South East recorded a 1.9% annual fall to £383,573.

London’s homeowners saw values decline by 1.2% to £536,751.

Housing market slowdown

Amanda Bryden, the head of mortgages at Halifax, said: “The recent slowdown in the housing market reflects the wide uncertainty regarding the conflict in the Middle East.

“Concerns about higher energy prices have pushed up inflation expectations, which in turn led to a rise in mortgage rates, reducing confidence that interest rates will be cut this year and dampening the initial momentum in the market seen at the start of the year.”

She added: “The effect on house prices will largely depend on how long-lasting these pressures prove to be and the wider implications for the economy and unemployment.

“However, the recent increase in UK mortgage rates has been more modest than the sharp rises seen during the mini budget of 2022.”

Property sector reaction

Nathan Emerson, the CEO of Propertymark, said: “We are at an important intersection where we must clearly acknowledge future challenges ahead.

“We started the year with positivity in terms of seeing an uplift in the average number of viewings per available property, coupled with general consumer positivity regarding affordability.

“However, a lot has changed in a short space of time, with numerous sub 4% mortgage deals being withdrawn over the last few weeks as the wider economy adjusts to potential uncertainties.”

Karen Noye, a mortgage expert at Quilter, said: “Looking ahead, the path for house prices will depend largely on how the conflict evolves.

“If tensions ease and energy‑driven inflation pressures recede, mortgage rates could stabilise and drift lower again, supporting broadly flat prices.

“If the conflict drags on, persistently higher mortgage rates are more likely to translate into weaker activity and softer prices, particularly in more rate‑sensitive parts of the market.”

Tom Bill, the head of UK residential research at Knight Frank, said: “What goes up must come down, but for mortgage rates the drop will be more gradual than the sharp increase triggered by the Middle East conflict, even if the two-week ceasefire deal holds.

“Sentiment in the housing market will improve if the war stops, but its longer-term inflationary impact and weaker demand for UK government debt due its tight financial headroom and apparent inability to cut spending means mortgage rates won’t snap back to where they were in February. This will keep demand and house prices in check this year.”

Jason Tebb, president of OnTheMarket, said: “The momentum created by several interest rate reductions over the past year and a half, combined with post-Budget clarity, continues to be in evidence on the ground, with needs-driven buyers and sellers who have put moves on hold focused on transacting.

“With further rate reductions on hold for the short term at least, and the threat of rate rises a concern the longer the conflict in the Middle East continues, those with competitive mortgage offers are keen to proceed before rates edge higher.”

The post House prices dip in March as annual growth also slows appeared first on Property118.

View Full Article: House prices dip in March as annual growth also slows

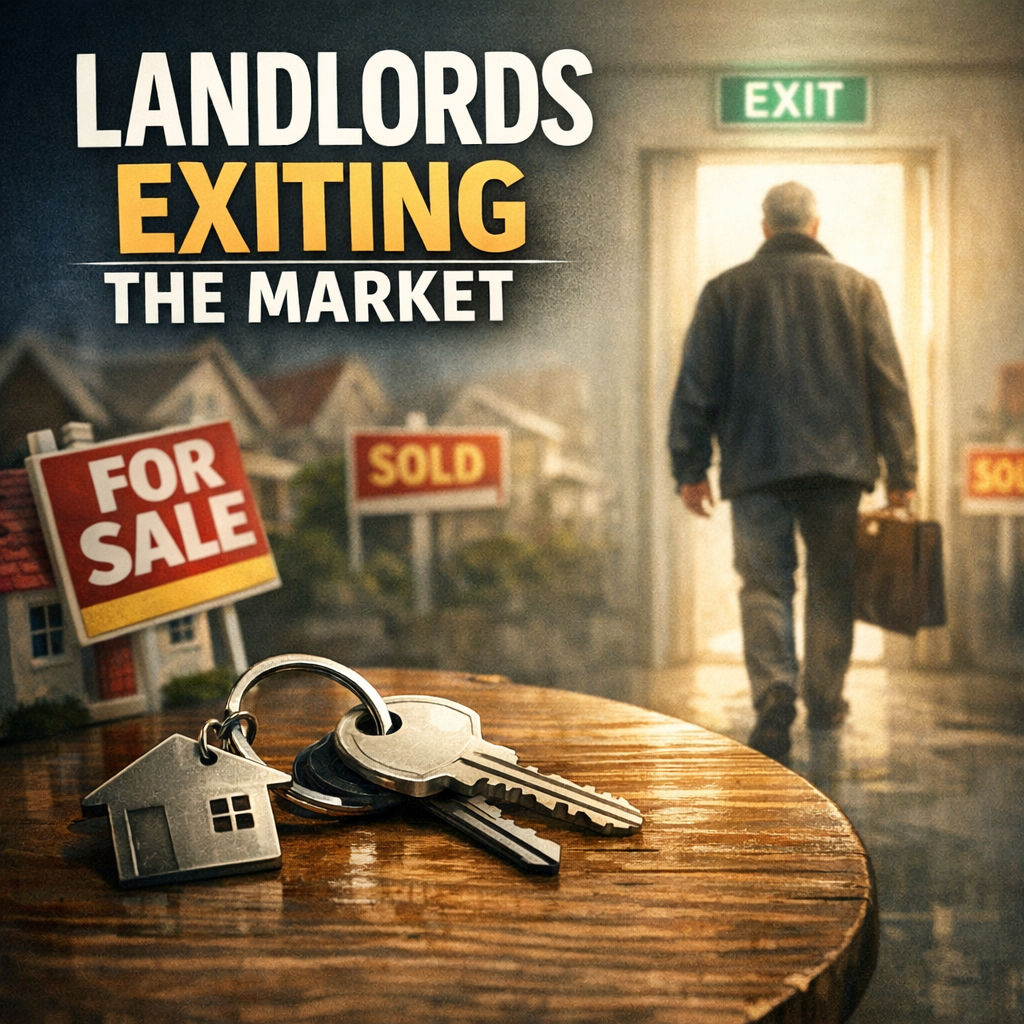

Nearly 1 in 5 landlords planning to exit the market entirely

Property118

Nearly 1 in 5 landlords planning to exit the market entirely

A more concerning signal is now emerging from the UK private rented sector, and it goes beyond portfolio adjustments. According to the Property118 Landlord Sentiment Survey Q1 2026, a significant proportion of landlords are not simply reducing their exposure, they are considering leaving the market altogether.

Based on 2,380 completed responses, nearly one in five landlords indicated that they are planning a full exit from the sector. You can review the full dataset here.

The implication is clear: this is not just a rebalancing, it is a withdrawal.

A quiet but meaningful shift

Much of the public discussion around landlords has focused on regulatory change, tax pressure and tenant protections. What has been less visible is how landlords are actually responding in practice. This data provides a clearer answer.

While some landlords are choosing to hold or gradually reduce their portfolios, a notable proportion have reached a different conclusion. Rather than adapting further, they are choosing to step away entirely.

This is not happening loudly, and it is not being driven by panic. It is happening quietly, through individual decisions that, when viewed collectively, begin to form a clear pattern.

Who is leaving, and why it matters

The survey shows that the landlord base is heavily weighted towards older investors, with the majority aged 56 and above. This context matters when interpreting exit intentions.

For many, the decision to leave is not reactive, it is rational. After decades of building portfolios, many landlords are now reassessing whether the current environment justifies continued involvement. Regulatory complexity, shifting tax treatment and changing risk dynamics all play a role, but the underlying driver is often simpler; control. At a certain stage, landlords begin to prioritise certainty and simplicity over further growth.

Not distress, but decision

One of the more revealing aspects of the survey findings is that many of those considering exit are not highly leveraged. A large proportion of respondents report loan-to-value ratios below 50%, with a significant number owning properties outright. This suggests that exits are not being forced by financial pressure, but chosen as part of a wider strategic reassessment. This distinction is important because it points to a sector where experienced landlords are stepping back not because they have to, but because they want to.

Implications for housing supply

If even a portion of these intended exits materialise, the impact on housing supply could be significant. Properties leaving the rental sector do not automatically return as rental stock. In many cases, they are sold to owner-occupiers, reducing the number of homes available to rent. At the same time, as highlighted in the wider survey results, relatively few landlords are planning to expand. The combination of these two forces, increased exits and limited new investment, creates a clear directional pressure.

A turning point, not a temporary phase

This survey represents the first in a planned quarterly series, meaning these findings provide an early indication of sentiment rather than a one-off snapshot. However, the scale of the response and the consistency of the data suggest that this is not a temporary fluctuation. It may instead represent the early stages of a broader transition in how landlords engage with the private rented sector.

For now, one conclusion stands out: a growing proportion of landlords are not adjusting their strategy, they are choosing to leave the market altogether.

A conversation worth having?

If you are weighing up your own strategy, whether that’s to sell, expand, or restructure to improve profitibility, it is worth having a discussion with a Property118 consultant to take a closer look at how your portfolio is structured as a whole now, and to forecast the outcomes based on multiple scenario’s.

These conversations are typically most useful for landlords with established portfolios and relatively modest borrowing who are beginning to reflect on how their assets could work more effectively in the years ahead.

/* “function”==typeof InitializeEditor,callIfLoaded:function(o){return!(!gform.domLoaded||!gform.scriptsLoaded||!gform.themeScriptsLoaded&&!gform.isFormEditor()||(gform.isFormEditor()&&console.warn(“The use of gform.initializeOnLoaded() is deprecated in the form editor context and will be removed in Gravity Forms 3.1.”),o(),0))},initializeOnLoaded:function(o){gform.callIfLoaded(o)||(document.addEventListener(“gform_main_scripts_loaded”,()=>{gform.scriptsLoaded=!0,gform.callIfLoaded(o)}),document.addEventListener(“gform/theme/scripts_loaded”,()=>{gform.themeScriptsLoaded=!0,gform.callIfLoaded(o)}),window.addEventListener(“DOMContentLoaded”,()=>{gform.domLoaded=!0,gform.callIfLoaded(o)}))},hooks:{action:{},filter:{}},addAction:function(o,r,e,t){gform.addHook(“action”,o,r,e,t)},addFilter:function(o,r,e,t){gform.addHook(“filter”,o,r,e,t)},doAction:function(o){gform.doHook(“action”,o,arguments)},applyFilters:function(o){return gform.doHook(“filter”,o,arguments)},removeAction:function(o,r){gform.removeHook(“action”,o,r)},removeFilter:function(o,r,e){gform.removeHook(“filter”,o,r,e)},addHook:function(o,r,e,t,n){null==gform.hooks[o][r]&&(gform.hooks[o][r]=[]);var d=gform.hooks[o][r];null==n&&(n=r+”_”+d.length),gform.hooks[o][r].push({tag:n,callable:e,priority:t=null==t?10:t})},doHook:function(r,o,e){var t;if(e=Array.prototype.slice.call(e,1),null!=gform.hooks[r][o]&&((o=gform.hooks[r][o]).sort(function(o,r){return o.priority-r.priority}),o.forEach(function(o){“function”!=typeof(t=o.callable)&&(t=window[t]),”action”==r?t.apply(null,e):e[0]=t.apply(null,e)})),”filter”==r)return e[0]},removeHook:function(o,r,t,n){var e;null!=gform.hooks[o][r]&&(e=(e=gform.hooks[o][r]).filter(function(o,r,e){return!!(null!=n&&n!=o.tag||null!=t&&t!=o.priority)}),gform.hooks[o][r]=e)}});

/* ]]> */

Enquire about a free initial discussion with a Property118 consultant

-

Mr.Mrs.MissMs.Dr.Prof.Rev.

-

-

Important Notice – Scope of Planning Support

Where our recommendations touch on areas requiring regulated input, we refer clients to appropriately authorised professionals for advice and implementation.

-

-

-

/* = 0;if(!is_postback){return;}var form_content = jQuery(this).contents().find(‘#gform_wrapper_585′);var is_confirmation = jQuery(this).contents().find(‘#gform_confirmation_wrapper_585′).length > 0;var is_redirect = contents.indexOf(‘gformRedirect(){‘) >= 0;var is_form = form_content.length > 0 && ! is_redirect && ! is_confirmation;var mt = parseInt(jQuery(‘html’).css(‘margin-top’), 10) + parseInt(jQuery(‘body’).css(‘margin-top’), 10) + 100;if(is_form){jQuery(‘#gform_wrapper_585′).html(form_content.html());if(form_content.hasClass(‘gform_validation_error’)){jQuery(‘#gform_wrapper_585′).addClass(‘gform_validation_error’);} else {jQuery(‘#gform_wrapper_585′).removeClass(‘gform_validation_error’);}setTimeout( function() { /* delay the scroll by 50 milliseconds to fix a bug in chrome */ }, 50 );if(window[‘gformInitDatepicker’]) {gformInitDatepicker();}if(window[‘gformInitPriceFields’]) {gformInitPriceFields();}var current_page = jQuery(‘#gform_source_page_number_585′).val();gformInitSpinner( 585, ‘https://www.property118.com/wp-content/plugins/gravityforms/images/spinner.svg’, true );jQuery(document).trigger(‘gform_page_loaded’, [585, current_page]);window[‘gf_submitting_585′] = false;}else if(!is_redirect){var confirmation_content = jQuery(this).contents().find(‘.GF_AJAX_POSTBACK’).html();if(!confirmation_content){confirmation_content = contents;}jQuery(‘#gform_wrapper_585′).replaceWith(confirmation_content);jQuery(document).trigger(‘gform_confirmation_loaded’, [585]);window[‘gf_submitting_585′] = false;wp.a11y.speak(jQuery(‘#gform_confirmation_message_585′).text());}else{jQuery(‘#gform_585′).append(contents);if(window[‘gformRedirect’]) {gformRedirect();}}jQuery(document).trigger(“gform_pre_post_render”, [{ formId: “585”, currentPage: “current_page”, abort: function() { this.preventDefault(); } }]); if (event && event.defaultPrevented) { return; } const gformWrapperDiv = document.getElementById( “gform_wrapper_585″ ); if ( gformWrapperDiv ) { const visibilitySpan = document.createElement( “span” ); visibilitySpan.id = “gform_visibility_test_585″; gformWrapperDiv.insertAdjacentElement( “afterend”, visibilitySpan ); } const visibilityTestDiv = document.getElementById( “gform_visibility_test_585″ ); let postRenderFired = false; function triggerPostRender() { if ( postRenderFired ) { return; } postRenderFired = true; gform.core.triggerPostRenderEvents( 585, current_page ); if ( visibilityTestDiv ) { visibilityTestDiv.parentNode.removeChild( visibilityTestDiv ); } } function debounce( func, wait, immediate ) { var timeout; return function() { var context = this, args = arguments; var later = function() { timeout = null; if ( !immediate ) func.apply( context, args ); }; var callNow = immediate && !timeout; clearTimeout( timeout ); timeout = setTimeout( later, wait ); if ( callNow ) func.apply( context, args ); }; } const debouncedTriggerPostRender = debounce( function() { triggerPostRender(); }, 200 ); if ( visibilityTestDiv && visibilityTestDiv.offsetParent === null ) { const observer = new MutationObserver( ( mutations ) => { mutations.forEach( ( mutation ) => { if ( mutation.type === ‘attributes’ && visibilityTestDiv.offsetParent !== null ) { debouncedTriggerPostRender(); observer.disconnect(); } }); }); observer.observe( document.body, { attributes: true, childList: false, subtree: true, attributeFilter: [ ‘style’, ‘class’ ], }); } else { triggerPostRender(); } } );} );

/* ]]> */

|

★★★★★

|

Help other landlords find Property118If you have found Property118 useful, a short Trustpilot review would make a meaningful difference. It helps other landlords decide whether our research is worth following. |

The post Nearly 1 in 5 landlords planning to exit the market entirely appeared first on Property118.

View Full Article: Nearly 1 in 5 landlords planning to exit the market entirely

Tenant starts fight with management?

Property118

Tenant starts fight with management?

My rental tenant of eight years has got herself into a nasty fight with the managing agent of the development. The dispute concerns the new electronic gates of this gated development, which management says she deliberately damaged and was observed doing so.

Apparently, this happened back in January, but I was only contacted about it by email last night (2 April). They are insisting I pay up (amount unspecified as yet) for the repairs as I am her landlord and so ultimately responsible according to my lease.

I immediately forwarded the email to my tenant and asked her to explain. She replied that she has proof in her “records” that she was not at fault and will supply this to me at a future date. She also denies another vague charge from management that she deliberately “fly tipped” a bed frame on the site (the matter is “under investigation”). She even said she would take legal action against this second accusation if necessary.

I am quite shocked by all this, as my tenant works as a diplomat, and such behaviour seems out of character. She does have a boyfriend who lives with her part of the time. The management company is relatively new and does have a habit of sending out regular complaint emails to owners and tenants about everything from parking to satellite dishes to the electronic gates in question, which now require quite a complex procedure of digital key fobs and codes to gain entry to the site.

This is worrying as I am planning to sell the flat this summer (I have not told my tenant yet) and cannot afford to have an ongoing dispute with management, putting off potential buyers. I also do not want to pay what sounds like an escalating bill for this problem. My tenant gets a high salary and also benefits from diplomatic immunity, so I just want her to pay up for the damage ASAP and not cause me any more problems.

But she seems to want to fight management over this. Any advice from anyone?

Thanks,

Helen

The post Tenant starts fight with management? appeared first on Property118.

View Full Article: Tenant starts fight with management?

Categories

- Landlords (19)

- Real Estate (9)

- Renewables & Green Issues (1)

- Rental Property Investment (1)

- Tenants (21)

- Uncategorized (12,638)

Archives

- April 2026 (63)

- March 2026 (72)

- February 2026 (55)

- January 2026 (52)

- December 2025 (62)

- August 2025 (51)

- July 2025 (51)

- June 2025 (49)

- May 2025 (50)

- April 2025 (48)

- March 2025 (54)

- February 2025 (51)

- January 2025 (52)

- December 2024 (55)

- November 2024 (64)

- October 2024 (82)

- September 2024 (69)

- August 2024 (55)

- July 2024 (64)

- June 2024 (54)

- May 2024 (73)

- April 2024 (59)

- March 2024 (49)

- February 2024 (57)

- January 2024 (58)

- December 2023 (56)

- November 2023 (59)

- October 2023 (67)

- September 2023 (136)

- August 2023 (131)

- July 2023 (129)

- June 2023 (128)

- May 2023 (140)

- April 2023 (121)

- March 2023 (168)

- February 2023 (155)

- January 2023 (152)

- December 2022 (136)

- November 2022 (158)

- October 2022 (146)

- September 2022 (148)

- August 2022 (169)

- July 2022 (124)

- June 2022 (124)

- May 2022 (130)

- April 2022 (116)

- March 2022 (155)

- February 2022 (124)

- January 2022 (120)

- December 2021 (117)

- November 2021 (139)

- October 2021 (130)

- September 2021 (138)

- August 2021 (110)

- July 2021 (110)

- June 2021 (60)

- May 2021 (127)

- April 2021 (122)

- March 2021 (156)

- February 2021 (154)

- January 2021 (133)

- December 2020 (126)

- November 2020 (159)

- October 2020 (169)

- September 2020 (181)

- August 2020 (147)

- July 2020 (172)

- June 2020 (158)

- May 2020 (177)

- April 2020 (188)

- March 2020 (234)

- February 2020 (212)

- January 2020 (164)

- December 2019 (107)

- November 2019 (131)

- October 2019 (145)

- September 2019 (123)

- August 2019 (112)

- July 2019 (93)

- June 2019 (82)

- May 2019 (94)

- April 2019 (88)

- March 2019 (78)

- February 2019 (77)

- January 2019 (71)

- December 2018 (37)

- November 2018 (85)

- October 2018 (108)

- September 2018 (110)

- August 2018 (135)

- July 2018 (140)

- June 2018 (118)

- May 2018 (113)

- April 2018 (64)

- March 2018 (96)

- February 2018 (82)

- January 2018 (92)

- December 2017 (62)

- November 2017 (100)

- October 2017 (105)

- September 2017 (97)

- August 2017 (101)

- July 2017 (104)

- June 2017 (155)

- May 2017 (135)

- April 2017 (113)

- March 2017 (138)

- February 2017 (150)

- January 2017 (127)

- December 2016 (90)

- November 2016 (135)

- October 2016 (149)

- September 2016 (135)

- August 2016 (48)

- July 2016 (52)

- June 2016 (54)

- May 2016 (52)

- April 2016 (24)

- October 2014 (8)

- April 2012 (2)

- December 2011 (2)

- November 2011 (10)

- October 2011 (9)

- September 2011 (9)

- August 2011 (3)

Calendar

Recent Posts

- Why some North West family homes are attracting stronger demand than landlords expect

- Selling with tenants in place may be easier than you think

- James Cleverley blames Labour’s Renters’ Rights Act after receiving Section 21 notice

- Landlords reducing exposure as regulatory pressure reshapes behaviour

- Sky News Section 21 story suggests a deeper problem to me