Instant Conveyancing Quote

admin

admin

Competitive Conveyancing from our preferred partner

We have teamed up with The Moving Hub to bring you competitive conveyancing quotes for your house purchase, sale or remortgage for Buy to Let or your main residence.

As members of Property118, you will have exclusive access to the following:

- Competitive and instant fixed fee conveyancing quotes

- Access to solicitors nationwide

- A team that will help you work with the right solicitor for your case

- No hidden charges or unknown extras

- Buyer Protection insures you for up to £2250 in your conveyancing , survey and mortgage fees should the property fall through

- All solicitors are regulated by the same service level agreement to ensure a consistent conveyancing service

- Support 24/7 from The Moving Hub

Click Here for a conveyancing quote

The post Instant Conveyancing Quote appeared first on Property118.

View Full Article: Instant Conveyancing Quote

Generation Rent are more reliant than ever on the PRS

A survey carried out by LetBritain of 2000 UK adults shows that 39% are financial unable to purchase the home they would like and are reliant on the Private Rental Sector (PRS) to meet their needs.

In London this jumps to a whopping 49% who are unable to purchase, because of the disparity in house prices.

In a bizarre twist opposed to government policy, 27% of adults renting said they were looking to purchase a Buy to Let property to get on the housing ladder. In London 42% of renters said they would consider purchasing a Buy to Let in more affordable areas of the country.

61% of those surveyed said they blamed the government for not doing enough to help Generation Rent and 64% said they could only see the situation getting worse in the next five years.

LetBritain CEO, Fareed Nabir, added “With more and more people across the UK coming to rely on the private rental sector, the results of the research are concerning. Whilst many renters are working hard to enter the property market, they clearly do not feel the government understands the issues faced by tenants.”

“Interestingly, the findings show that Generation Rent is now increasingly looking to buy properties outside of their chosen place of residence so they can still get onto the property ladder without having to sacrifice the location or quality of the property they wish to live in.”

The post Generation Rent are more reliant than ever on the PRS appeared first on Property118.

View Full Article: Generation Rent are more reliant than ever on the PRS

We Should Be Using Net Rental Yields

I have just responded to a Facebook post by axe the tenant tax, the post was about landlords losing confidence with rental profits. The article ended with the fact that rental yields are holding up at 6% I have done some calculations and would like those good at the maths to make comment or provide alternative figures. I believe that net rental profits are down to average of 2%

Too much talk about rental yields that are gross figures ie 6%, due to the recent government taxes we should now quote net yield for greater accurately. Paying tax has now become a cost of doing business due to the loss of interest as an expense.

I did a calculation based on an average property price of £190,000, average rent of £850 per month, average loan of 60%, average interest rate of 4.5%, average running costs which included full management or an employed team for the larger landlord like myself of which costs 30% of the rent if you do your figures right, I allocated 5% of the rent for capital improvements or to go into a sinking fund for long term improvements.

The figures I came out with were that 25% of the rent goes to the tax man, 25% pays the interest on loans, 5% to the sinking fund, 30% to running costs (which includes repairs, administration costs, management for all new rules and regulations), this left 15% after tax profit for the landlord.

Now at £850 per month that’s £10,200 per year and 15% of that = £1,530 after tax profit per year.

Now let’s forget the capital appreciation because no one includes that in working out the yields, capital employed and put into the purchase of the property is 40% of £190,000 = £76,000 and the return on investment for £1,530 after tax rent on our cash investment of £76,000 = 2.01%

So big difference from the quoted figures of 6%

Any one any comments.

The post We Should Be Using Net Rental Yields appeared first on Property118.

View Full Article: We Should Be Using Net Rental Yields

What is a Section 20 Notice ?

There are two instances of section 20 notices in property in England:

(1) is the notice served in relation to early shorthold tenancies under the Housing Act 1988, and the other,

(2) refers to section 20 of the Landlord and Tenant Act 1985, as amended by the Commonhold and Leasehold Reform Act (CLRA) 2002, which involves leasehold property and consultation with leaseholders on major works.

Housing Act 1988 – Shorthold Tenancies

Prior to 28 February 1997 shorthold tenancies were not automatic (the default tenancy) as they have been for residential tenancies since the amendment brought in by the Housing Act 1996, (effective February 1997) but had to be created by informing the tenant by a prescribed form statutory notice – the section 20 notice.

A landlord wishing to create an assured shorthold tenancy was required to serve a notice under s20 of the Housing Act 1988 before the tenancy was entered into.

If the notice was not properly served (i.e. before the agreement was signed) the tenancy could not be an assured shorthold. In default it became an ordinary assured tenancy which gives the tenant security of tenure. Landlords in this position therefore could not use the not fault, s21 eviction process.

There cannot be many tenancies around dating from pre February 1997 which needed a s20 notice serving at the time, but where they do exist, landlords are unable to evict these tenants unless they can prove a s20 notice was properly served prior to the tenancy. Landlords or agents at the time would normally get the tenant to sign a statement to this effect.

Since 28 February 1997 it has not been necessary to serve a s20 notice for the tenancy to be an assured shorthold tenancy (AST).

Many mistakes were made in respect of s20 notices and many lawyers have since paid for their holidays by challenging them in possession claims.

The most common problem with this was the inability of the landlord or agent to prove that the s20 notice was served prior to the grant of the tenancy, but also in some cases the notice was not in the prescribed form.

Section 20 of the 1988 Act required the notice to be in the prescribed form stipulated in the Assured Tenancies and Agricultural Occupancies (Forms) Regulations 1988 (as amended). The relevant form was Form No.7

Landlord and Tenant Act 1985 – consultation with leaseholders on major works

Section 20 (s20) is a clause in the Landlord and Tenant Act 1985 which is intended to protect leaseholders from paying unnecessarily large sums for work carried out to their building. In effect it says that a leaseholder’s contribution to the cost of works will be capped if the landlord or their managing agent fails to follow a set consultation process.

Section 20 of the Landlord & Tenant Act 1985 (as amended by the Commonhold & Leasehold Reform Act 2002) sets out a three-stage consultation process which must be followed when carrying out qualifying works to a building where the contribution from any one lessee exceeds £250, or a qualifying long-term agreement where the contribution from any one lessee exceeds £100 in one financial year.

Stage One – s20

For qualifying works, under Section 20 managing agents / freeholders must serve a “Notice of Intention to Carry Out Works” on all lessees.

This Notice must generally describe the proposed works, state the reasons for considering the proposed works, and invite leaseholders to make written observations within 30 days.

It is a requirement that a correspondence address for these observations be stated within the s20 notice. The Notice of Intention offers lessees the opportunity to provide the name of a contractor from whom the landlord, managing agents or Resident’s Management Committee (RMC) can try to obtain estimates for the proposed works.

Stage Two – s20

At the expiration of the 30 day consultation period, at least two estimates should be obtained: one of these estimates must be from a person completely independent of the landlord, the managing agent or the RMC.

If nominations were made within the consultation period, then estimates should have been obtained from at least one of these nominations. The landlord/agent/RMC must then provide a “Statement of Estimates” which will set out the details of estimates that have been obtained and a summary of observations received within the consultation period.

All estimates obtained must be made available for inspection by the lessees, including estimates obtained from nominated contractors.

A “Notice to Accompany the Statement of Estimates” must also be served in conjunction with the Statement of Estimates, which sets out the hours involved, and a place where details of the estimates may be inspected, again inviting lessees to make written observations on the estimates within 30 days, and specifying the address to which those observations should be sent.

Stage Three – s20

If, at the expiration of the consultation period, the chosen contractor did not provide the lowest estimate, then a “Notice of Reasons” must be served upon all lessees.

This means that the landlord/agent/RMC must state the reasons for awarding the contract where they do not opt for the lowest estimate.

The nomination is open to a test of reasonableness by the Leasehold Valuation Tribunal (LVT) under Section 19 of the 1985 Landlord & Tenant Act.

Where it can be shown that the consultation procedure is not followed correctly, and the landlord/agent/RMC is successfully challenged at the LVT, then the maximum amount recoverable from lessees under the service charge is £250 for major works and £100 for long-term agreements.

For more information on Section 20 lease matters see these guides:

– The Association of Residential Managing Agents (ARMA) – Advice Note Section 20 Consultation and Major Works – a guide to the S.20 consultation process for major works and long term agreements.

– The Leashold Advisory Service – What is the Section 20 consultation process for major works?

©1999 – Present | Parkmatic Publications Ltd. All rights reserved | LandlordZONE® – What is a Section 20 Notice ? | LandlordZONE.

View Full Article: What is a Section 20 Notice ?

Derelict pub converted into a flat, modern HMO and commercial unit

In this case study, learn how long term Shawbrook Bank customer HMO Property Investments Ltd used finance to transform a derelict pub into a thriving new mixed use property in Lincoln, with Shawbrook Broker and Property118 Partner Brooklands Commercial Finance acting as intermediary.

If you are considering a refurb, development or commercial project it is definitely worth watching the video below to see how one of our favourite banks helped the clients with Bridging facilities and then switching straight to a term mortgage.

If you require assistance with any type of property finance from Buy to Let mortgages, commercial mortgages, Development finance and Refurbs to Bridging finance for investors and developers please complete the contact form below and we will be pleased to get our team at Brooklands Commercial finance to help.

jQuery(document).bind(‘gform_post_render’, function(event, formId, currentPage){if(formId == 209) {} } );jQuery(document).bind(‘gform_post_conditional_logic’, function(event, formId, fields, isInit){} ); jQuery(document).ready(function(){jQuery(document).trigger(‘gform_post_render’, [209, 1]) } );

The post Derelict pub converted into a flat, modern HMO and commercial unit appeared first on Property118.

View Full Article: Derelict pub converted into a flat, modern HMO and commercial unit

Advice – Tenants subletting on AirBnB

It appears I had a tenant subletting my property for bed and breakfast on AirBnB.

I recently had a battle to evict a tenant that ran the duration right up until bailiff attendance. The property was let through a letting agent. The story was that the guy was splitting from his wife and leaving the marital home (owned) and needed a place fairly local. He rented a 4 bed from me so that his children would be able to stay over. The guy produced bank statements showing 70+k in his account as he was a self-employed tree surgeon and his books didn’t reflect his earnings accurately. All other references checked out.

I got a bit uncomfortable during the stage when negotiating the initial AST rent, he seemed quite aggressive. I got even more worried when he failed to attend the agent’s office to collect the keys but made some excuse and asked if he could collect them from us after hours. A car with 4 Chinese people turned up on our doorstep at gone 8.30 pm asking for the keys. On calling the letting agent on his mobile he explained it away as his wife collecting the keys for him.

Later, after the initial 12 months the agent broached the matter of a rent review which was met with fierce resistance, so advised the agent I wasn’t comfortable with his general attitude and to serve a S21. The minute this was done he phoned the branch manager and was arguing aggressively; during that conversation he completely changed tac. He immediately revealed his knowledge about eviction procedure and told the agent he wasn’t moving out without bailiffs. No further rent was received from then on, it turned out he had never changed the bills into his name, he was switched to a key meter 3 months before final eviction but had never topped up (later found the electric bypassed), socket faces removed and extension leads hard-wired in etc. etc.

The long and the short is that he owed far more than the deposit covered in arrears, costs and damages. Fortunately I had rent guarantee insurance to mitigate the arrears but am having to go through Small Claims Court for the rest.

After bringing the property back up to standard, we secured a new tenant and the property is let once again.

Tonight we received a message from the tenant stating that someone had turned up on the doorstep claiming to have booked bed and breakfast and got very grumpy when turned away, claiming that he had stayed there before.

With this knowledge I Googled bed and breakfast in Basingstoke; AirBnB popped up, so I zoomed in on the map and low and behold there was a room advertised for £27 a night right where my property would be. The description made note that the address had changed. There was even mention of the tenant in the feedback comments, so I opened up the cached pages and there it was, my property address was actually mentioned in the advert. From reading the comments it appears that the pair of them are doing this across a number of properties in the south and London.

What should I do? Involve the Housing Officer at the Council? Is there legal action that I can take? Is Police intervention required? Should I involve Inland Revenue? Is there any action I can take via Small Claims Court?

Any advice would be greatly appreciated.

Thank you

André

The post Advice – Tenants subletting on AirBnB appeared first on Property118.

View Full Article: Advice – Tenants subletting on AirBnB

LSE call on Chancellor to reform Stamp duty

The London School of Economics and the VATT Institute for Economic have produced a research paper predicting the level of home moving would increase by 27% if the Stamp duty levy was completely abolished.

The research indicates current levels of stamp duty are making the housing crisis worse by cause a bottleneck in the market with pensioners being deterred form downsizing by the costs and stalling families from purchasing larger homes.

The Chancellor Philip Hammond is reportedly under pressure from his own Cabinet to reform Stamp Duty to kick start the market, which is also a major contributor to the wider economy. It is thought from a previous reform that if you halved the tax then income to the treasury would actually increase.

Co-author of the report, Professor Christian Hilber, said: “The key message of our paper is that stamp duty hampers mobility significantly.

“If you are a young family and you have an additional child, you’ll need an additional room, but the stamp duty is discouraging this kind of move because of the additional cost and lack of available homes to move into.

“In a nutshell, the stamp duty discourages the elderly from downsizing and young expanding families from moving to more adequate larger housing.”

Former chancellor, Lord Lawson of Blaby, told the Telegraph: “The present levels of stamp duty are clearly counterproductive, in terms of housing policy and revenue alike, and need to be reduced. For what it’s worth, when I was Chancellor, I halved the rate of stamp duty on house sales, and the revenue increased.”

HM Treasury replied saying: “Almost 90% of people want to own a home, but only 63% do. We reformed property taxes including stamp duty to help more people get onto the property ladder.

“In addition, we are helping people, including young families, to buy their first homes through policies such as Help to Buy and the Lifetime ISA, and the recent £2.3bn Housing Infrastructure Fund which will free up over 100,000 properties in high demand areas.”

| Purchase price of property | Rate of Stamp Duty | Buy to Let/ Additional Home Rate |

|---|---|---|

| £0 – £125,000 | 0% | 3% |

| £125,001 – £250,000 | 2% | 5% |

| £250,001 – £925,000 | 5% | 8% |

| £925,001 – £1.5 million | 10% | 13% |

The post LSE call on Chancellor to reform Stamp duty appeared first on Property118.

View Full Article: LSE call on Chancellor to reform Stamp duty

Are you properly alarmed?

Smoke and Carbon Monoxide Alarm Regulations:

From 1 October 2015, the law changed regarding smoke and carbon monoxide (CO) detectors and you may need reminding of the regulations as they now stand.

From that date, landlords in England are required to have fitted smoke detectors (alarms) on each storey of a rental property. CO detectors are also required in rooms where solid fuel appliances (e.g. those containing an open fire or log-burning stove) are installed.

Although not a legal requirement in the case of gas appliances, the Department of Communities and Local Government (DCLG) has said that it would expect and encourage reputable landlords to ensure that working CO alarms are installed. Landlords with properties in England must now fit these devices and not wait for the start of a new tenancy. Heat detectors designed for kitchens cannot be a substitute for smoke alarms.

Since 1 June 1992 Approved Document B (Fire Safety), which supports the Building Regulations (England and Wales) 2010, has required all new build properties to have hard- wired smoke alarms on at least each storey of the property. However, until now there was no requirement to have smoke alarms in older and non-licensed dwellings.

New requirements

At least one smoke alarm must be installed on each storey of a rental property used as living accommodation, and a CO alarm in any room containing solid fuel appliances that is used as living accommodation. After that, the landlord must make sure the alarms are in working order at the start of each new tenancy. Note: in the DCLG’s view, for the purpose of these regulations, a mezzanine floor would not be considered a storey.

In general, smoke alarms should be fixed to the ceiling in a circulation space, i.e. a hall or a landing, and CO alarms should be positioned at head height, either on a wall or shelf, approximately 1‒3m away from a potential source.

The immediate landlord (or someone acting on their behalf) must test the alarms on the first day of a new tenancy, ideally with the tenant/s present. Tenants should be advised to take responsibility for their own safety and test all alarms regularly to make sure they are in working order; testing monthly is generally considered an appropriate frequency.

The first day of the tenancy is the date stipulated in the agreement, even where the tenant decides to actually move into the property on a later date. A new tenancy is one commencing after the 1 October 2015, not a continuation of an existing tenancy before that date.

In cases where tenants refuse access for alarm fitting or testing, the landlord should write to them, with a copy to the local authority, explaining that it is a legal requirement to install the alarms and that it is for their own safety.

The regulations do not stipulate the type of alarms (such as hard wired or battery powered) to be installed. Landlords should make an informed decision and choose the best alarms for their properties and tenants, but it is recommended that 10-year guarantee lithium battery or hard-wired alarms are installed in pre-1 June 1992 properties.

The regulations will apply to any tenancy, lease or licence (not lodgers living with a landlord and family) of residential premises in England, that gives somebody the right to occupy all or part of the premises as their only or main residence, in return for rent. There are some exemptions, such as for long leaseholds and social housing landlords.

Documentary evidence

Landlords and/or their managing agents should ensure that they have documentary evidence that the alarms are tested and in working order on the first day of a tenancy, for example, by the tenant signing a copy of an inventory. Failure to comply with these regulations would mean the local housing authority can levy a civil penalty charge of up to £5,000 on the landlord, but there is a right of appeal.

Landlords and managing agents are encouraged to ensure tenants’ safety and provide documentary evidence of this by carrying out basic risk assessments covering fire, gas, electrical, Legionella and general safety inside and outside the property between each tenancy.

Regulations vary throughout the UK and there is some overlap. This is a brief summary:

Wales: The new regulations do not apply here, but similar rules are expected soon. Currently, properties in Wales built post-1992 must be fitted with mains-powered, interlinked smoke detectors/alarms, but landlords are advised to provide at least battery-operated alarms in older properties. Houses in multiple occupation (HMOs) are required to have hard-wired alarms fitted.

In England and Wales there is also a duty under the Part J of the 2010 Building Regulations for England and Wales to have CO alarms fitted when a solid fuel heating system is installed – Building Regulations 2010 – Combustion Appliances

Scotland: The mandatory fitting of CO alarms in private rented property became law on 14 May 2014 under the Housing Scotland Act 2014 (http://bit.ly/VPf2dJ). Besides existing gas safety regulations, the act prescribes that there must be “satisfactory provision for giving warning if CO is present in a concentration hazardous to health”.

This means that it is now mandatory for private landlords to install CO detectors in every space containing a ‘fixed combustion appliance’ (excluding those used solely for cooking) and where a flue passes through high-risk accommodation, such as a bedroom or main living room.

On 1 December 2015, new regulations came into force regarding the provision of long-life CO alarms in privately rented housing. This addition to the Housing (Scotland) Act is an amendment to the existing Repairing Standard that firmly shifts the duty of care regarding the provision and replacement of CO detectors to landlords. The legislation applies to all landlords in Scotland renting out property with fixed combustion appliances of any kind, with the exception of those used exclusively for cooking.

Fire safety (smoke alarms) revised guidance in Scotland www.prhpscotland.gov.uk makes it mandatory that one fire and smoke detector alarm is fitted:

- in the room most frequently used by the occupant(s) for general daytime living purposes

- in every circulation space (halls and landings)

- on each floor of a building

- in every kitchen.

All alarms must be integrated.

Northern Ireland: Technical Document L of the Building Regulations in Northern Ireland states: “Where any combustion appliance is installed, reasonable provision must be made to detect and give warning of the presence of CO gas at levels harmful to people. The authority for this is that landlords of private rental properties (that are not HMOs) are required, within reason, to ensure that the property they let is ‘safe and would not cause injury or death to humans or pets’.” Landlords must therefore be able to prove due diligence in a court of law should a fire occur at the property.

The Northern Ireland Fire and Rescue Service (NIFRS) recommend that the standards of fire safety in private rental properties should be at least equivalent to the current fire safety standards expected in a modern domestic property. Therefore, landlords renting a private property should at least provide working smoke alarms (preferably interconnected) on each level of the property and detection in the principal habitable room, considered to be the main living room, and a heat detector and fire blanket in the kitchen area.

Guidance concerning smoke and CO alarms is available from the NIFRS at: www.nifrs.org/fire-safety/community-information-bulletins

The Smoke and Carbon Monoxide Alarm (England) Regulations 2015

©1999 – Present | Parkmatic Publications Ltd. All rights reserved | LandlordZONE® – Are you properly alarmed? | LandlordZONE.

View Full Article: Are you properly alarmed?

Can investors still make money from Buy to Let

Can investors still make money from investing in buy to let property with all the restrictions that have been placed on the industry?

In the recent budget announcement (2016) landlords could quite easily be left with a feeling that they have been targeted because of the previous Mortgage tax relief changes and investor Stamp Duty. Investors can no longer claim tax relief on all their mortgage interest payments, which means that if previously they were making a net profit of £10,000 per annum but was paying £5,000 in mortgage interest costs, they could wipe that off and only pay tax on the remaining £5,000. The changes mean that higher-rate taxpayers whose mortgage interest costs make up 75% or more of their rental income will see their profits completely wiped out.

It is understandable that both new and seasoned investors alike might be put off from investing in property. There are various solutions available that can help you maximise profits and ensure that you are getting the best value for money. Below are some suggestions that can help you make money in the buy to let property market.

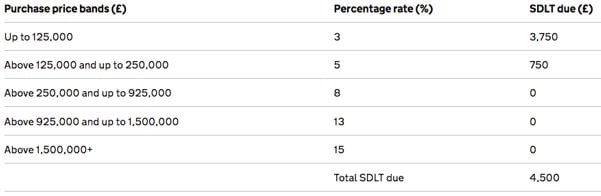

Reduce the cost of purchasing a property

In April 2016 additional stamp duty charges were announced, which means that landlords must pay an extra 3% in stamp duty charges. With average house prices in the north west at £186k and west midlands at £213k according to Rightmove’s House Price Index, on a buy-to-let investment of £140,000 that means a whopping £4,500 in Stamp Duty.

https://www.tax.service.gov.uk/calculate-stamp-duty-land-tax/#/detail

Understandably, this has deterred investors from considering buy-to-let property, however there are alternative options that allow investors to mitigate their loss. Commercial property investments such as Care home investments and student property investments with values under £150,000, have NO stamp duty. Several investors are realising the benefits of these opportunities because the savings on Stamp Duty increases their yield on cost and ultimately the return on investment. Individuals have the potential to save thousands of pounds, simply by reconsidering the asset type they choose to own.

Research the most suitable areas for the asset class

The best areas for investment can be dependent upon the type of property you are wanting to purchase. For example, a sleepy town in the south west of England might be perfect for a care home investment, but not so suitable for a student accommodation investment.

For buy to let investments specifically, you should weigh up each area’s credentials in terms of its demographics, regeneration projects, vicinity to large cities (or whether the development is in a large city itself), transport links, employment options and comparable developments in the area. This research can be time consuming and for busy working professionals they find they cannot always afford the time to conduct such extensive research. Many employ the help of an investment company who have taken the leg work out of the research and who can provide guidance to investors.

Know the realistic rental yield that can be achieved

Achieving a good rental yield is a fine balancing act. For example, in London house prices are high so the average rental yield is around 4.4%. Compare that with the North West where property is typically cheaper and you are looking at returns of 6.4% on average, and according to Rightmove’s Rental Trends Tracker, Liverpool can achieve some of the highest yields in the country at 6.7%. This is all a balancing act though, as if you choose to buy a property at a rock-bottom price you may find that there is very little demand for the property, or that the rent generated from the property’s occupancy is disappointing. According to LendInvest, other areas that investors can expect a high yield include Peterborough, Stevenage and Rochester.

This leads us perfectly to our next point, which can have a knock-on effect with regards to how much rent per calendar month you can charge tenants.

Choose buy-to-let investments in areas experiencing regeneration

Investing in property in an area experiencing regeneration has many benefits, and one if which is that property prices are still reasonable but are predicted to increase in value once the regeneration is complete. This allows investors to either increase rent after a set period which has a knock-on effect on the annual rental yield, but it also means that they can sell on the property at a higher price, resulting in good capital uplift. The benefit of investing in an up-and-coming area is the increase in demand from young professionals, looking to move to the area in pursuit of fresh opportunities and jobs. Over the past twenty years, two London boroughs that have been particularly appealing to young professionals – Hackney and Haringey – have experienced the highest growth in terms of house prices at 749% and 544% respectively. They have all experienced regeneration and gentrification too, due to young professionals being priced out of the more expensive Shoreditch area.

Consider the condition of the property

Beautiful Georgian and Victorian buildings capture the hearts of most people. However, they are more likely to need significant repair work and care to make them attractive to the rental market. The cost that goes into renovating the development could seriously deplete profit margins, and may mean that the landlord will have to check up on the property and make improvements more often than with a new build. A building requiring a lot of maintenance will not only affect the rental yields, but also will mean that the investor would have to invest a significant amount of time to the property’s upkeep.

One Touch Property can help you take a decision on what would work best for your financial expectations. Whether it be a buy to let property investment or a different asset class, One Touch Property offers different types of investments to suit every individual’s needs.

jQuery(document).bind(‘gform_post_render’, function(event, formId, currentPage){if(formId == 403) {} } );jQuery(document).bind(‘gform_post_conditional_logic’, function(event, formId, fields, isInit){} ); jQuery(document).ready(function(){jQuery(document).trigger(‘gform_post_render’, [403, 1]) } );

The post Can investors still make money from Buy to Let appeared first on Property118.

View Full Article: Can investors still make money from Buy to Let

Lost deeds from 1956?

A solicitor has been holding the deeds to my father in laws house since 1956. He has now moved into a nursing home so there is now a need to put it on the market and sell it.

However, it now turns out the solicitor could not find the deeds and they say they gave them to a third party in 1978 who was negotiating a £3000 advance. This person cannot be found and solicitor has no proof of releasing Deeds.

Land registry will not give full title deeds only possessory title because of this and the solicitor refuses to except any responsibility for loss are there any other avenues other then taking legal action open to us.

Many thanks

Steve

The post Lost deeds from 1956? appeared first on Property118.

View Full Article: Lost deeds from 1956?

Categories

- Landlords (19)

- Real Estate (9)

- Renewables & Green Issues (1)

- Rental Property Investment (1)

- Tenants (21)

- Uncategorized (12,523)

Archives

- March 2026 (20)

- February 2026 (55)

- January 2026 (52)

- December 2025 (62)

- August 2025 (51)

- July 2025 (51)

- June 2025 (49)

- May 2025 (50)

- April 2025 (48)

- March 2025 (54)

- February 2025 (51)

- January 2025 (52)

- December 2024 (55)

- November 2024 (64)

- October 2024 (82)

- September 2024 (69)

- August 2024 (55)

- July 2024 (64)

- June 2024 (54)

- May 2024 (73)

- April 2024 (59)

- March 2024 (49)

- February 2024 (57)

- January 2024 (58)

- December 2023 (56)

- November 2023 (59)

- October 2023 (67)

- September 2023 (136)

- August 2023 (131)

- July 2023 (129)

- June 2023 (128)

- May 2023 (140)

- April 2023 (121)

- March 2023 (168)

- February 2023 (155)

- January 2023 (152)

- December 2022 (136)

- November 2022 (158)

- October 2022 (146)

- September 2022 (148)

- August 2022 (169)

- July 2022 (124)

- June 2022 (124)

- May 2022 (130)

- April 2022 (116)

- March 2022 (155)

- February 2022 (124)

- January 2022 (120)

- December 2021 (117)

- November 2021 (139)

- October 2021 (130)

- September 2021 (138)

- August 2021 (110)

- July 2021 (110)

- June 2021 (60)

- May 2021 (127)

- April 2021 (122)

- March 2021 (156)

- February 2021 (154)

- January 2021 (133)

- December 2020 (126)

- November 2020 (159)

- October 2020 (169)

- September 2020 (181)

- August 2020 (147)

- July 2020 (172)

- June 2020 (158)

- May 2020 (177)

- April 2020 (188)

- March 2020 (234)

- February 2020 (212)

- January 2020 (164)

- December 2019 (107)

- November 2019 (131)

- October 2019 (145)

- September 2019 (123)

- August 2019 (112)

- July 2019 (93)

- June 2019 (82)

- May 2019 (94)

- April 2019 (88)

- March 2019 (78)

- February 2019 (77)

- January 2019 (71)

- December 2018 (37)

- November 2018 (85)

- October 2018 (108)

- September 2018 (110)

- August 2018 (135)

- July 2018 (140)

- June 2018 (118)

- May 2018 (113)

- April 2018 (64)

- March 2018 (96)

- February 2018 (82)

- January 2018 (92)

- December 2017 (62)

- November 2017 (100)

- October 2017 (105)

- September 2017 (97)

- August 2017 (101)

- July 2017 (104)

- June 2017 (155)

- May 2017 (135)

- April 2017 (113)

- March 2017 (138)

- February 2017 (150)

- January 2017 (127)

- December 2016 (90)

- November 2016 (135)

- October 2016 (149)

- September 2016 (135)

- August 2016 (48)

- July 2016 (52)

- June 2016 (54)

- May 2016 (52)

- April 2016 (24)

- October 2014 (8)

- April 2012 (2)

- December 2011 (2)

- November 2011 (10)

- October 2011 (9)

- September 2011 (9)

- August 2011 (3)

Calendar

Recent Posts

- Gen Z renters lack knowledge of credit scores and rent rules

- Google searches for Making Tax Digital hit record high

- The Property118 Housing Research Panel

- Are tenants beginning to see the problem of landlords leaving?

- Councils collect just 25% of landlord fines