Bristol Slum Landlords Exploiting Migrants…

admin

admin

Rouge Landlords:

Slum landlords who have been exploiting migrants in shocking housing conditions are to be targeted by a new Bristol Council inspection team says the Bristol Post. The scheme to crack down on these landlords is being funded by central government.

The team aims to inspect thousands of privately-rented homes across the Bristol city. This comes after a whole host of “shocking conditions” have been exposed over the past few months by the Bristol Post.

Funding provided by The Home Office will be used by the Council – more than £320,000 – from a ‘Controlling Migration Fund’ to be used solely to tackle the “decrepit state” of many privately-rented homes and rooms in certain parts of the city.

Poor standards housing is a recognised issue across Bristol, but it is thought to be markedly worse in places with concentrated populations of migrants and refugees. Unscrupulous ‘rouge landlords’ are said to rely on the fact people who are relatively new to the country either don’t know they can complain about it, or are afraid to.

The council says that migrants are ‘over-represented in the private rented sector’ in Bristol. This is because they are at the bottom of the queue for council housing, often ending up in properties in poor condition.

Over the past year, the Bristol Post has exposed a housing crisis in the city. It has revealed stories such as that of the Somali woman whose neighbours of 12 years in Easton lined up to prevent a ‘revenge eviction’, instigated by here complaining about damp.

There was another shocking example with the death of Jorge Rias, a Colombian who died in a single room in a House in Multiple Occupancy (HMO) in St Paul’s that was so smelly, his body wasn’t discovered for weeks.

Recently the Post exposed how one landlord told another family from overseas, whose children have been born and grown up in Bristol, that they would be evicted after they complained of water pouring down walls when it rains.

Those kinds of anecdotal evidence are said to be multiplied countless times across the city. A situation that has prompted central government to fund Bristol to the tune of £321,750 for a two-year project to identify and target these rogue landlords, and where necessary to take enforcement action.

Bristol’s housing chief, Cllr Paul Smith has said:

“Across the city people are finding it increasingly difficult to access decent, affordable homes.

“In Bristol we are working hard to tackle criminal landlords and through this extra funding, we expect to see a reduction in the number of these criminal landlords letting out poor quality accommodation and exploiting tenants.

“Making sure that everyone in Bristol has a safe, comfortable place to call home, is one of our key priorities, and we are doing all we can to make this a reality. We intend to use all enforcement powers at our disposal where appropriate,” Cllr Smith added.

Controversy has surrounded the government’s ‘Controlling Migration Fund’ as it often leads to enforcement action being taken against people who are found to be in the country illegally.

The fund is actually split into two parts: one half is to tackle the illegal immigrants, and the second to help authorities assist those people who are here quite legally and this is where the money to target slum landlords is to come from.

The councils says that this money will pay for around 1,200 inspections of properties in Bristol.

©1999 – Present | Parkmatic Publications Ltd. All rights reserved | LandlordZONE® – Bristol Slum Landlords Exploiting Migrants… | LandlordZONE.

View Full Article: Bristol Slum Landlords Exploiting Migrants…

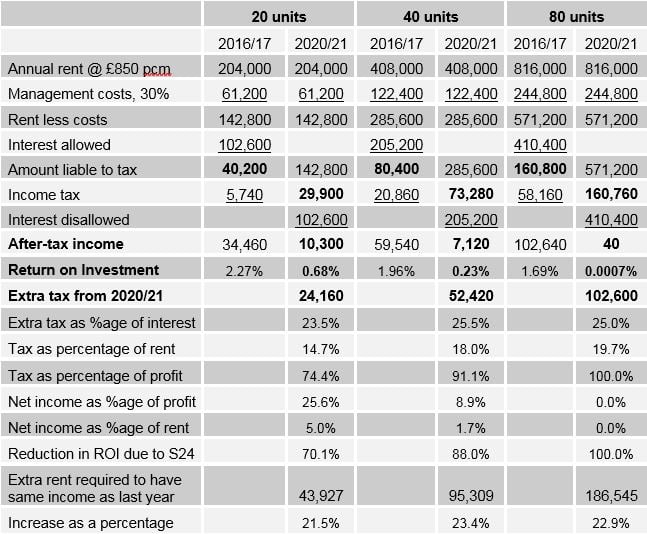

The paradox of Section24

Last week a reader pointed out that the gross yield figures that are bandied about are misleading and we should concentrate on the return on investment (ROI).

https://www.property118.com/using-net-rental-yields/

The gross yield is the annual gross rent as a percentage of the value of the property. The ROI is the after-tax profit as a percentage of the amount invested, basically the deposit where a mortgage is involved.

He did a calculation based on the following average figures: property price £190,000, rent £850 per month, loan 60%, interest rate of 4.5%,running costs which included full management or an employed team for the larger landlord like himself which costs 30% of the rent. He arrived at an ROI of 2.01%. The gross yield is 5.4%

The consensus was that ROI is much more useful. And somebody pointed out that we now have to take S 24 into account as it dramatically reduces after-tax profit where finance costs are incurred.

He asked readers to check his calculation. Using the above figures per unit I tried to calculate how many units he had in order to arrive at an ROI of 2.01%. Assuming that there were no joint owners, and he had no other income, the answer is nearer 40 than 20.

This calculation revealed a paradox. Normally you would expect a bigger portfolio to produce a bigger after-tax income in absolute terms, and this is what happened until last year. As the table shows, after tax income does not exactly double as the number of units doubles, but it grows from £34k to 60k to £103k

However, under S 24, after-tax income will go down in absolute terms as the size of the portfolio doubles, from £10k to £7k to almost nothing – 50p per property per year.

At 81 units the tax will exceed 100% of the real profit.

And at each size, the fictitious profit will rule out entitlement to any benefits.

The owner’s work will just be for the benefit of his tenants, his employees, his lenders and his government.

I then calculated what effect S 24 would have on ROI as from 2020/21 when it is fully phased in. At 20 units it will be reduced by seven-tenths. At 40 units it will be reduced by nine-tenths. At 80 units it will be extinguished.

The effect of Section 24 of the Finance (No.2) Act 2015 on different sizes of portfolio

The real profit figures are on the line “Amount liable to tax” in the columns headed 2016/17

The extra tax is about 45% on the interest, minus the 20% “relief”.

To avoid bankruptcy he needs to increase the rent. He should have started to do so before April when S24 began to be phased in. To maintain the same after-tax income as he had last year he will need to increase the rent by the above percentages before April 2020, from £850 to about £1,050.

It is not sufficient to increase rents by the amount of extra tax because the increase itself will be taxed at 45%.

I have assumed that his 30% management costs do not include any agents fees that would go up in line with rents. If there are, he will have to increase rents even more

The post The paradox of Section24 appeared first on Property118.

View Full Article: The paradox of Section24

A few questions on a development opportunity we have

Hello All!

My wife and I are pursuing a development plot nearby where we live in Manchester and I’d like to ask readers for their thoughts on a few issues.

We’d like to develop 1 or 2 properties on this site.

We currently own a couple of BTLs and our own home all of which are mortgaged. We have the cash to buy the site (unless it goes for well over the asking price) and we have also set up a property SPV in advance of this type of opportunity. Our questions:

- Ownership – should we buy the site personally or through a Ltd company? Can we transfer into company at later stage? What is stamp duty?

- Financing – should we use self build mortgage, development finance, what gearing? Is development finance as easy to get through company as personally? Would having some of our money covering the development costs make much difference? to either the rate or our overall lendability?

- What’d we do with profits? – take out? reinvest in more property? pay down lending? And what are tax considerations of each?

- What we’d do with properties? – We’re not sure whether we’d rent out, sell, or even possibly live in them?

- Tax management – capital gains, reinvestment, Stamp Duty. Do we pay tax if profits are reinvested in property through Ltd company?

Any thoughts on any of these issues and what advice we should be seeking would be most helpful.

Many thanks in advance.

All best

Andy

The post A few questions on a development opportunity we have appeared first on Property118.

View Full Article: A few questions on a development opportunity we have

Property fraudsters stealing homes

Home owners and buy-to-let landlords are being warned of a potential rise in property fraudsters activity. This is more prevalent during the summer house marketing season.

This alert comes from Midlands property lawyer Javed Ahmed who says that owners could find themselves conned out of hundreds of thousands of pounds by people who “clone” their identities and sell houses and flats out from under them.

Mr Ahmed, from Midlands law firm mfg Solicitors, is concerned there will be a rise in fraud over the summer – typically the busiest time for the property market – and said owners needed to act now to protect themselves.

The assistant solicitor said fraudsters operating across the region had even been known to fool estate agents and lawyers by posing as the owner of property and then managing to take out loans or mortgage the building without the real owner’s knowledge.

Mr Ahmed said:

“Property is usually the most valuable asset people will own and it’s a hugely attractive target for fraudsters who want to sell it and pocket the money.

“It is something people think will never happen to them but it is a very real threat and people here in the Midlands must guard against it.

“Those who are most at risk are people who rent out their property, or whose property is vacant.

“It’s particularly an issue for those who own the property outright without a mortgage but one of the best steps is for owners to arrange a restriction on their title to prevent the Land Registry registering a sale without the identities being verified…”

Ahmed says this is a process best taken care of by a professional to ensure every box is ticked.

Mr Ahmed has produced guidance on the issue which advises people on a variety of ways to protect themselves and their property. This includes:

- Ensuring the property is registered at HM Land Registry

- Be part of HM Land Registry’s monitoring service to ensure you are notified of any suspicious activity involving the property

- Updating the property address with HM Land Registry should it be sold.

Javed Ahmed, Assistant Solicitor can be reached at mfg Solicitors on 0845 55 55 321 or javed.ahmed@mfgsolicitors.com

Protect your land and property from fraud

Property Alert Service – Land Registry

©1999 – Present | Parkmatic Publications Ltd. All rights reserved | LandlordZONE® – Property fraudsters stealing homes | LandlordZONE.

View Full Article: Property fraudsters stealing homes

Sale and Rent Back Court Case Wreaks Havoc

A couple who purchased their neighbour’s house to help him out of financial difficulty 20 years ago have been ordered by a judge to give him a 90 year lease at a fixed rent of only £800 for the whole term.

David and Sheila Harding who purchased the property from their neighbour Colin Gregory now want to sell to fund a new life in Spain, but in the possession hearing were branded by the judge as “foolhardy in the extreme” and refused permission to appeal.

Mr Gregory told his neighbours, the Hardings, of his difficulties in paying his mortgage. To assist the Hardings purchased his property for £143,000 in 2001 with a “Buy to Rent” mortgage allowing Mr Gregory to stay in his home at an agreed rent of £800pcm.

The property was recently offered back Mr Gregory to purchase for £60,000 less than the now £310,000 value and he was given a year to find the funds, which he was unable to do.

The Hardings eventually found a buyer that agreed to continue renting to Mr Gregory at an increased rate of £1,200. This was refused by Mr Gregory and the case went to Brighton County Court in March 2016 where Mr Gregory said he sold the house to the Hardings for a reduced price, only because he could rent it for as long as he wanted.

We have not seen the actual tenancy agreement, but there was apparently no mention of the life time occupation and fixed rental in the documents.

The decision by the Judge will also adversely affect the security of the lender, who could well force a sale through LPA receivers for breach of contract with a 90 year lease. The property could be valued as little as 20 times rent (£800 x12x20 =£192,000), which is roughly what freehold ground rents trade at

The case was won by Mr Gregory’s solicitor using two extremely old pieces of law which included:

- The 1925 Property Act under which he apparently has the right to pay £800 for the next 90 years.

- The 1948 Bannister v Bannister case where a woman was given the right to live rent free for life in a cottage she sold to her brother for under market value.

The Hardings were ordered to pay Mr Gregory’s costs of £11,000 and they can now only sell the property to a buyer prepared to rent to Mr Gregory for 90 years at £800 pcm.

Although the Judge refused the right to appeal Property118 was also refused this by Mr Justice Teare in our case against West Brom. Mark Smith (Barrister-at-Law) then won the right and Mr Justice Teare was proved wrong by our later win in the Court of Appeal.

There is a process to take this further, but it depends on what the tenancy agreement says and if it is an AST or an Assured tenancy. Even if the landlord hadn’t properly served s13 he had the right to do so. Surely, that alone would be grounds for an application to appeal?

If anyone out there knows the Hardings please get them to contact Property118 so we can investigate if there is the possibility to win a right to appeal. Time is of the essence!

We also need to ascertain how many Sale and Rent Back (SARB) agreements and mortgages this case could affect in the future as a precedent.

Mr Harding said after the case, “‘We tried to help out, not only as a good neighbour and landlord, but we considered Colin a good friend.

“We own it, we pay the mortgage on it, we bought it but due to a nearly 100 year old law he gets to live in it on the cheap. We have nowhere to turn to and can’t believe it has turned out like this.

“We went into court told by our solicitors that there would be no problem and walked out with him winning the case and us owing him costs. It’s ludicrous. There is nothing more we can do.

“We want to warn other people who are thinking of entering into any kind of agreement like this. We did everything by the book and look where it ended up.

“Nobody had ever heard of the law the solicitor used but it has cost us dearly. We’re stuffed!”

The post Sale and Rent Back Court Case Wreaks Havoc appeared first on Property118.

View Full Article: Sale and Rent Back Court Case Wreaks Havoc

Beware BICT Copycats

There are now several ‘copy-cat’ structures which appear very similar to the BICT “Beneficial Interest Company Transfer” structure being offered by tax-planners but many of them do not obtain non-statutory clearance.

BICT is a legal structure which enables landlords to avoid the costs associated with refinancing at the point of incorporation. It has no tax advantages but it does afford an opportunity to keep attractive mortgage facilities in place.

However, when BICT is done badly it can have dire tax consequences.

We have mystery-shopped some of the copy-cat companies and it is very clear that they are offering extremely dangerous advice, in that the structures they are promoting fall short of delivering all of the promises they make. For example, some are transferring beneficial interest using a Deed of Trust but are completely overlooking the importance of a professionally drafted Business Sale Agreement and a Clearing Agency Contract between the company and the mortgage borrower. Many lenders will not accept mortgage payments from companies, hence the payments are being made to the landlord who in turn pays the mortgage. This is fine in principle, but there could be major tax consequences if the paperwork is wrong or if there isn’t any at all. We suspect many of the landlords using these ‘copy-cat’ schemes will find that their mortgage payments will be deemed to be income paid to them by their company and taxed accordingly by HMRC, which is very worrying indeed.

We think one of the reasons Property118 Limited has been so successful of late has been due to our fee charging structure in regards to assisting with non-statutory clearance applications. Our fee is just £1,500 + VAT but that is refunded in full if clearance is declined. That peace-of-mind seems to be making all the difference.

Incorporation using the BICT structure is only one of the tax planning strategies recommended by Property118 Limited. This is because there is no ‘one-size-its-all’ solution. For this reason, an initial consultation is required to establish the current position and future aspirations of clients prior to an analysis and a detailed written report being prepared and followed up with a telephone or Skype based Q&A session. Clients of Property118 Limited are encouraged to include their accounts in this process and this in turn often leads to those accountants referring more of their clients. The fee for these consultations is £400 and comes with a guarantee of total satisfaction or a full refund.

The legal work associated with the implementation of BICT incorporation is always referred by Property118 Limited to Cotswold Barristers where clients own properties in England & Wales. For clients in Scotland, an Edinburgh legal firm provides additional assistance in regards to preparing the paperwork and dealing with LBTT returns, which are invariably £nil for business partnerships.

Mark Smith, Head of Chambers at Cotswold Barristers said; “we are delighted with the symbiotic relationship with Property118 Limited and the work flowing therefrom. We reciprocate wherever possible and fully anticipate the number landlords using the BICT strategy for incorporation to continue to increase”

The post Beware BICT Copycats appeared first on Property118.

View Full Article: Beware BICT Copycats

Beware Tax Planning Models Using LLP’s

If you are being advised to use an LLP as a stepping stone towards incorporation then you have good cause to be wary.

There is a business model which is doing the rounds at the moment which relies on a piece of legislation which was created to deal with CGT on the liquidation of an LLP. However, this legislation is being abused and in my opinion it will not be long before HMRC comes down on it like a ton of bricks under their General Anti Abuse Rules in GAAR legislation.

When property is transferred into an LLP there can be no SDLT or CGT payable. That is a fact.

It is also a fact that if the partnership geuinly fails and is liquidated then the base costs for calculating CGT is the value of the properties at the point they were transferred into the LLP.

At face value this is all great news because at the time the properties are transferred to the LLP they may well be worth considerably more than they cost to acquire.

However, if you enter into a LLP with the sole intention of liquidating it at a later date to avoid tax that is without doubt abuse of the tax system and HMRC are going to be far from happy about it. My concern is that 1,00’s of LLP’s are currently being formed for exactly that purpose.

It doesn’t take a rocket scientist to see how HMRC will see straight though this.

If you form an LLP today, liquidate it after say one year and then a company, which has exactly the same owners miraculously decides to acquire the same assets it is pretty obvious what has occurred.

If this structure has pitched to you please consider very carefully what I have said above. You could find an unwelcome tax demand on your doormat for all the CGT you have avoided at some point in the weeks, months or even years after you have liquidated.

Show Tax Consultation Booking Form

The post Beware Tax Planning Models Using LLP’s appeared first on Property118.

View Full Article: Beware Tax Planning Models Using LLP’s

Devon landlord receives prison sentence for unsafe DIY gas work

Gas Safe:

Allan King an Ilfracombe landlord was given a suspended jail term plus a £14,000 fine for endangering the lives of his tenants with DIY gas work in his rental property.

Exeter Crown Court on 4th August heard that in September 2016 King replaced a boiler himself at his rented property on Arcade Road, this despite have no training in gas work and not being registered with the Gas Safe Register.

After the boiler developed a fault a month after the fitting, King called in a gas engineer for assistance. The engineer immediately recognised the DIY botch job and realised the boiler was risking the tenants’ lives, so he isolated. Following this The Health and Safety Executive (HSE) was informed and it launched an investigation.

It seems that King had had a previous warning in July 2016 from The HSE that only a member of Gas Safe Register is allowed to work on gas appliances.

King of Arcade Road, Ilfracombe pleaded guilty to breaches of the Gas Safety (Installation and Use) Regulations 1998 and the Health and Safety at Work Act 1974. He was sentenced to nine months imprisonment suspended for 18 months and fined £3,000. He was also ordered to pay costs of £12,184.14.

HSE Inspector, Simon Jones, speaking after the hearing, said:

“Landlords have a legal duty to ensure that any gas work at their rented properties is only undertaken by a member of Gas Safe Register.

“In this case, Mr King ignored previous warnings and undertook his own DIY gas work for which he had neither the competence nor credentials.”

”His actions were dangerous and put his tenants’ lives at risk’

A Landlord’s Responsibilities with Gas:

When letting a property that contains gas and gas appliances (including lodgers in a landlord’s own home) these precautions must be followed by law:

- Make sure gas fittings, flues and appliances are installed and maintained in a safe condition in accordance with the manufacturer’s service instructions. If these are not available it is recommended that they are serviced annually, unless advised otherwise by a Gas Safe registered engineer

- Have an annual gas safety check carried out by a Gas Safe registered engineer on each gas appliance and flue and a Gas Safety Certificate issued.

- During the tenancy, or before any new tenancy starts, make sure the Gas Safety Certificate is current, and a copy is issued to the new or a current tenant within 28 days of the check

- The landlord to keep a record of each safety check for at least two years

Full information about landlords’ responsibilities for gas at: http://www.hse.gov.uk/gas/landlords/index.htm

A guide to landlords’ duties: Gas Safety (Installation and Use) Regulations 1998

©1999 – Present | Parkmatic Publications Ltd. All rights reserved | LandlordZONE® – Devon landlord receives prison sentence for unsafe DIY gas work | LandlordZONE.

View Full Article: Devon landlord receives prison sentence for unsafe DIY gas work

Are CHL’s mortgage terms reasonable or even legal?

Over the last 18 months I have had to point out to many of my consultancy clients that CHL “Capital Homeloans” are the only lender we are aware of which specifically prohibits the transfer of beneficial interest in their mortgage T&C’s.

This causes a major headache when if comes to tax planning strategies which rely on the use of Declarations of Trust.

I always make this clear to clients who have mortgages with CHL and point out that whilst the Declaration of Trust is completely invisible to anybody unless you declare it, the risk is that if a lender with such conditions in their T&C’s was to find out that technically you would be in default. However, there is no history of CHL or any other lender having ever called a loan in on this basis. Nor has there ever been a Court case where a lender has been granted possession or appointed LPA receivers for a breach of such conditions. Given that all conveyancing solicitors have at some point implemented Declarations of Trust you have to wonder why this is?

This also makes me wonder CHL’s conditions precluding the transfer of beneficial interest are reasonable or even legal.

What business is it of a mortgage lender who gets the benefit of capital appreciation and rental profits if it has no effect on their security whatsoever?

Show Tax Consultation Booking Form

The post Are CHL’s mortgage terms reasonable or even legal? appeared first on Property118.

View Full Article: Are CHL’s mortgage terms reasonable or even legal?

Headline Mortgage Rates for Limited Companies

Limited Company BTL mortgages are now available up to 85% LTV and rates start from 3.09%.

The buy-to-let market has been hit by numerous tax changes in the last couple of years. Two of the main ones being:

- the introduction of a 3% Stamp Duty surcharge

- Until April of this year private landlords could deduct both mortgage interest and other allowable costs, from their rental income before calculating the amount of tax due.

The restrictions on finance cost relief in particular has created a substantial increase in demand for Limited Company BTLs, which in turn has increased the number of lenders and products that are available for this market and this has caused a welcome reduction in the mortgage rates.

Before considering embarking on a purchase or re-mortgage in a Limited Company, the various Pro’s and Con’s should be considered:

Pros

- From 2017 to 2020, the amount of Buy to let tax relief that individual landlords can claim back will be cut from 45% to 20% for top rate taxpayers. This change does not affect Limited Companies.

- The first £5,000 of dividends is tax free, though this is likely to be reduced to £2,000.

- No income tax is payable when reinvesting profits to purchase further properties, although corporation tax is payable on trading profits.

- Limited Liability. If the company is dissolved then personal assets are protected (unless guarantees or other security is given)

- Properties within Limited Companies benefit from indexation allowances for the purpose of calculating capital gains whereas individuals get no such relief

- Incorporation relief can re-set the clock in terms of capital gains by washing them all into the value of shares created at the point of incorporation. Therefore, if the company was to sell a property the day after it acquired it there would be no tax to pay because there would be no capital gain. The historical capital gains on properties transferred into the company will only ever be paid if the shares in the company are sold. Once you die, any capital gains rolled into the shares dies too.

Cons

- No personal Capital Gains Tax (CGT) allowance when the company sells a property

- Transferring properties that are already owned by an individual into a Limited Company may be considered as a sale and purchase and may trigger a capital gains tax, stamp duty and re-mortgaging costs. Relief is available to mitigate these but only in certain circumstances. Seek professional guidance from Property118 on this point

The above is only an outline and professional advice should be taken for a competent commercial broker and specialist tax adviser.

As mentioned, the popularity of Limited Company BTLs has increased dramatically and this has increased the number of providers and products which has pushed down the costs, a trend that is quite likely to continue.

The differential in terms rates and LTVs for individuals and companies is narrowing on an ongoing basis.

In my next articles I will be looking at alternatives to traditional mortgage funding so please watch out for that.

jQuery(document).bind(‘gform_post_render’, function(event, formId, currentPage){if(formId == 214) {} } );jQuery(document).bind(‘gform_post_conditional_logic’, function(event, formId, fields, isInit){} ); jQuery(document).ready(function(){jQuery(document).trigger(‘gform_post_render’, [214, 1]) } );

The post Headline Mortgage Rates for Limited Companies appeared first on Property118.

View Full Article: Headline Mortgage Rates for Limited Companies

Categories

- Landlords (19)

- Real Estate (9)

- Renewables & Green Issues (1)

- Rental Property Investment (1)

- Tenants (21)

- Uncategorized (12,523)

Archives

- March 2026 (20)

- February 2026 (55)

- January 2026 (52)

- December 2025 (62)

- August 2025 (51)

- July 2025 (51)

- June 2025 (49)

- May 2025 (50)

- April 2025 (48)

- March 2025 (54)

- February 2025 (51)

- January 2025 (52)

- December 2024 (55)

- November 2024 (64)

- October 2024 (82)

- September 2024 (69)

- August 2024 (55)

- July 2024 (64)

- June 2024 (54)

- May 2024 (73)

- April 2024 (59)

- March 2024 (49)

- February 2024 (57)

- January 2024 (58)

- December 2023 (56)

- November 2023 (59)

- October 2023 (67)

- September 2023 (136)

- August 2023 (131)

- July 2023 (129)

- June 2023 (128)

- May 2023 (140)

- April 2023 (121)

- March 2023 (168)

- February 2023 (155)

- January 2023 (152)

- December 2022 (136)

- November 2022 (158)

- October 2022 (146)

- September 2022 (148)

- August 2022 (169)

- July 2022 (124)

- June 2022 (124)

- May 2022 (130)

- April 2022 (116)

- March 2022 (155)

- February 2022 (124)

- January 2022 (120)

- December 2021 (117)

- November 2021 (139)

- October 2021 (130)

- September 2021 (138)

- August 2021 (110)

- July 2021 (110)

- June 2021 (60)

- May 2021 (127)

- April 2021 (122)

- March 2021 (156)

- February 2021 (154)

- January 2021 (133)

- December 2020 (126)

- November 2020 (159)

- October 2020 (169)

- September 2020 (181)

- August 2020 (147)

- July 2020 (172)

- June 2020 (158)

- May 2020 (177)

- April 2020 (188)

- March 2020 (234)

- February 2020 (212)

- January 2020 (164)

- December 2019 (107)

- November 2019 (131)

- October 2019 (145)

- September 2019 (123)

- August 2019 (112)

- July 2019 (93)

- June 2019 (82)

- May 2019 (94)

- April 2019 (88)

- March 2019 (78)

- February 2019 (77)

- January 2019 (71)

- December 2018 (37)

- November 2018 (85)

- October 2018 (108)

- September 2018 (110)

- August 2018 (135)

- July 2018 (140)

- June 2018 (118)

- May 2018 (113)

- April 2018 (64)

- March 2018 (96)

- February 2018 (82)

- January 2018 (92)

- December 2017 (62)

- November 2017 (100)

- October 2017 (105)

- September 2017 (97)

- August 2017 (101)

- July 2017 (104)

- June 2017 (155)

- May 2017 (135)

- April 2017 (113)

- March 2017 (138)

- February 2017 (150)

- January 2017 (127)

- December 2016 (90)

- November 2016 (135)

- October 2016 (149)

- September 2016 (135)

- August 2016 (48)

- July 2016 (52)

- June 2016 (54)

- May 2016 (52)

- April 2016 (24)

- October 2014 (8)

- April 2012 (2)

- December 2011 (2)

- November 2011 (10)

- October 2011 (9)

- September 2011 (9)

- August 2011 (3)

Calendar

Recent Posts

- Gen Z renters lack knowledge of credit scores and rent rules

- Google searches for Making Tax Digital hit record high

- The Property118 Housing Research Panel

- Are tenants beginning to see the problem of landlords leaving?

- Councils collect just 25% of landlord fines