Property118 puts HMRC manual BIM45700 under FTT scrutiny

admin

admin

Property118

Property118 puts HMRC manual BIM45700 under FTT scrutiny

Since late 2023, HMRC has argued that financing the withdrawal of a positive capital account balance prior to incorporation of a business is a notifiable tax avoidance scheme under DOTAS legislation.

From our perspective, this makes no sense because that practice is supported by highly regarded industry textbook guidance published by Lexis Nexis, which says as follows …

Simon’s Taxes B9:114 – refinancing and ESC D32 considerations

If there is a substantial capital account in the unincorporated business, the business owner(s) should be advised to draw this down before incorporation, otherwise that capital will be locked into the value of the shares.

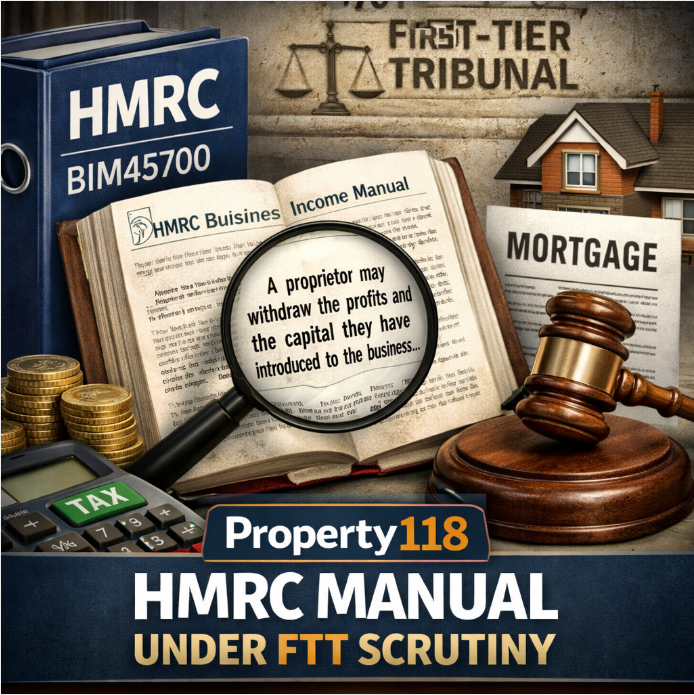

More importantly, HMRC’s own manual BIM45700 clearly states:

A proprietor of a business may withdraw the profits of the business and the capital they have introduced to the business, even though substitute funding then has to be provided by interest bearing loans. The interest payable on the loans is an allowable deduction. This is on the basis that the purpose of the additional borrowing is to provide working capital for the business. There will, though, be an interest restriction if the proprietor’s capital account becomes overdrawn, see BIM45705 onwards.

Source: https://www.gov.uk/hmrc-internal-manuals/business-income-manual/bim45700

HMRC has also recently taken the currently unpublished view (discovered via an FOI request) that if a company takes on new mortgages and uses those funds to redeem existing pre-incorporation mortgage liabilities, such funds could be treated as taxable consideration under CGT rules.

Important context: Property118 is not currently recommending Section 162 incorporation for landlords with mortgages while legal uncertainty remains over the treatment of mortgage liabilities. Read our current position here: Why Property118 is not currently recommending s162 incorporation to landlords with mortgages

The reason for our current position is not that the underlying principles are wrong, but that HMRC’s current interpretation conflicts with its own published guidance.

The above is intended to serve as a warning not only to landlords, but also to accountants, solicitors, barristers, mortgage brokers, lenders and financial advisers.

What our critics say

Some influencers have suggested that the timing of the financing of capital withdrawn, being so close to the date of incorporation, is abusive. We disagree on the basis that there is no evidence supported by legislation or HMRC manuals to support this stance, hence taking the case to the FTT.

They also argue that using the funds to loan to the company, immediately post-incorporation, and for the company to repay the debt quickly, is also abusive. Again, we disagree based on the same principles.

Finally, our critics have suggested that transferring only beneficial interest at incorporation is also abusive and constitutes a breach of mortgage terms, and that mortgage novation is the only acceptable method. Again, we disagree on the basis that it is common knowledge that taxation follows beneficial interest and that the Law of Property Act 1925 protects the interests of mortgage lenders even if liabilities are indemnified without the lender’s consent or knowledge. Furthermore, novation has not been mentioned in the relevant HMRC manuals since the phrase indemnity was introduced into them over 50 years ago, and in any event, very few, if any, mortgage lenders now offer novation.

Tribunal outcome

We expect the First-tier tribunal to make a ruling later this year, but the losing side could then appeal to the Upper Tribunal and beyond, resulting in the wait for much need clarity potentially being pushed back even further. Meanwhile, these matters continue to frustrate landlords who would like to incorporate their businesses for the reasons explained in HMRC’s GAAR Guidance Part D paragraph 2.2, as follows …

GAAR guidance – D2.2 intended legislative choice

D2.2

D2.2.1 This covers, for example, giving assets to children to reduce future Inheritance Tax liabilities, sacrificing salary in return for enhanced pension rights, disclaiming capital allowances to preserve reliefs for a later period, deciding to incorporate a business or to sell shares rather than assets (in both cases so as to pay less tax or Stamp Duty Land Tax) and choosing to borrow to invest in buy to let rather than using surplus cash or having a bigger mortgage on your main residence.

D2.2.2 These are all clearly things that are recognised by the statute: Parliament has given taxpayers a choice as to the course of action to take. This category might also include reorganising a trust or corporate structure in a straightforward way to fit in with a new tax regime.

The commercial reasons landlords choose to incorporate their rental property business were also documented in a report published by the Office of Tax Simplification in November 2022.

Source: https://www.gov.uk/government/publications/ots-review-of-residential-property-income

A conversation worth having?

If you are weighing up your own strategy, whether that’s to sell, expand, or restructure to improve profitability, it is worth having a discussion with a Property118 consultant to take a closer look at how your portfolio is structured as a whole now, and to forecast the outcomes based on multiple scenarios.

These conversations are typically most useful for landlords with established portfolios and relatively modest borrowing who are beginning to reflect on how their assets could work more effectively in the years ahead.

/* “function”==typeof InitializeEditor,callIfLoaded:function(o){return!(!gform.domLoaded||!gform.scriptsLoaded||!gform.themeScriptsLoaded&&!gform.isFormEditor()||(gform.isFormEditor()&&console.warn(“The use of gform.initializeOnLoaded() is deprecated in the form editor context and will be removed in Gravity Forms 3.1.”),o(),0))},initializeOnLoaded:function(o){gform.callIfLoaded(o)||(document.addEventListener(“gform_main_scripts_loaded”,()=>{gform.scriptsLoaded=!0,gform.callIfLoaded(o)}),document.addEventListener(“gform/theme/scripts_loaded”,()=>{gform.themeScriptsLoaded=!0,gform.callIfLoaded(o)}),window.addEventListener(“DOMContentLoaded”,()=>{gform.domLoaded=!0,gform.callIfLoaded(o)}))},hooks:{action:{},filter:{}},addAction:function(o,r,e,t){gform.addHook(“action”,o,r,e,t)},addFilter:function(o,r,e,t){gform.addHook(“filter”,o,r,e,t)},doAction:function(o){gform.doHook(“action”,o,arguments)},applyFilters:function(o){return gform.doHook(“filter”,o,arguments)},removeAction:function(o,r){gform.removeHook(“action”,o,r)},removeFilter:function(o,r,e){gform.removeHook(“filter”,o,r,e)},addHook:function(o,r,e,t,n){null==gform.hooks[o][r]&&(gform.hooks[o][r]=[]);var d=gform.hooks[o][r];null==n&&(n=r+”_”+d.length),gform.hooks[o][r].push({tag:n,callable:e,priority:t=null==t?10:t})},doHook:function(r,o,e){var t;if(e=Array.prototype.slice.call(e,1),null!=gform.hooks[r][o]&&((o=gform.hooks[r][o]).sort(function(o,r){return o.priority-r.priority}),o.forEach(function(o){“function”!=typeof(t=o.callable)&&(t=window[t]),”action”==r?t.apply(null,e):e[0]=t.apply(null,e)})),”filter”==r)return e[0]},removeHook:function(o,r,t,n){var e;null!=gform.hooks[o][r]&&(e=(e=gform.hooks[o][r]).filter(function(o,r,e){return!!(null!=n&&n!=o.tag||null!=t&&t!=o.priority)}),gform.hooks[o][r]=e)}});

/* ]]> */

Enquire about a free initial discussion with a Property118 consultant

-

Mr.Mrs.MissMs.Dr.Prof.Rev.

-

-

Important Notice – Scope of Planning Support

Important Notice – Scope of Planning SupportWhere our recommendations touch on areas requiring regulated input, we refer clients to appropriately authorised professionals for advice and implementation.

-

-

-

/* = 0;if(!is_postback){return;}var form_content = jQuery(this).contents().find(‘#gform_wrapper_585′);var is_confirmation = jQuery(this).contents().find(‘#gform_confirmation_wrapper_585′).length > 0;var is_redirect = contents.indexOf(‘gformRedirect(){‘) >= 0;var is_form = form_content.length > 0 && ! is_redirect && ! is_confirmation;var mt = parseInt(jQuery(‘html’).css(‘margin-top’), 10) + parseInt(jQuery(‘body’).css(‘margin-top’), 10) + 100;if(is_form){jQuery(‘#gform_wrapper_585′).html(form_content.html());if(form_content.hasClass(‘gform_validation_error’)){jQuery(‘#gform_wrapper_585′).addClass(‘gform_validation_error’);} else {jQuery(‘#gform_wrapper_585′).removeClass(‘gform_validation_error’);}setTimeout( function() { /* delay the scroll by 50 milliseconds to fix a bug in chrome */ }, 50 );if(window[‘gformInitDatepicker’]) {gformInitDatepicker();}if(window[‘gformInitPriceFields’]) {gformInitPriceFields();}var current_page = jQuery(‘#gform_source_page_number_585′).val();gformInitSpinner( 585, ‘https://www.property118.com/wp-content/plugins/gravityforms/images/spinner.svg’, true );jQuery(document).trigger(‘gform_page_loaded’, [585, current_page]);window[‘gf_submitting_585′] = false;}else if(!is_redirect){var confirmation_content = jQuery(this).contents().find(‘.GF_AJAX_POSTBACK’).html();if(!confirmation_content){confirmation_content = contents;}jQuery(‘#gform_wrapper_585′).replaceWith(confirmation_content);jQuery(document).trigger(‘gform_confirmation_loaded’, [585]);window[‘gf_submitting_585′] = false;wp.a11y.speak(jQuery(‘#gform_confirmation_message_585′).text());}else{jQuery(‘#gform_585′).append(contents);if(window[‘gformRedirect’]) {gformRedirect();}}jQuery(document).trigger(“gform_pre_post_render”, [{ formId: “585”, currentPage: “current_page”, abort: function() { this.preventDefault(); } }]); if (event && event.defaultPrevented) { return; } const gformWrapperDiv = document.getElementById( “gform_wrapper_585″ ); if ( gformWrapperDiv ) { const visibilitySpan = document.createElement( “span” ); visibilitySpan.id = “gform_visibility_test_585″; gformWrapperDiv.insertAdjacentElement( “afterend”, visibilitySpan ); } const visibilityTestDiv = document.getElementById( “gform_visibility_test_585″ ); let postRenderFired = false; function triggerPostRender() { if ( postRenderFired ) { return; } postRenderFired = true; gform.core.triggerPostRenderEvents( 585, current_page ); if ( visibilityTestDiv ) { visibilityTestDiv.parentNode.removeChild( visibilityTestDiv ); } } function debounce( func, wait, immediate ) { var timeout; return function() { var context = this, args = arguments; var later = function() { timeout = null; if ( !immediate ) func.apply( context, args ); }; var callNow = immediate && !timeout; clearTimeout( timeout ); timeout = setTimeout( later, wait ); if ( callNow ) func.apply( context, args ); }; } const debouncedTriggerPostRender = debounce( function() { triggerPostRender(); }, 200 ); if ( visibilityTestDiv && visibilityTestDiv.offsetParent === null ) { const observer = new MutationObserver( ( mutations ) => { mutations.forEach( ( mutation ) => { if ( mutation.type === ‘attributes’ && visibilityTestDiv.offsetParent !== null ) { debouncedTriggerPostRender(); observer.disconnect(); } }); }); observer.observe( document.body, { attributes: true, childList: false, subtree: true, attributeFilter: [ ‘style’, ‘class’ ], }); } else { triggerPostRender(); } } );} );

/* ]]> */

|

★★★★★

|

Help other landlords find Property118If you have found Property118 useful, a short Trustpilot review would make a meaningful difference. It helps other landlords decide whether our research is worth following. |

The post Property118 puts HMRC manual BIM45700 under FTT scrutiny appeared first on Property118.

View Full Article: Property118 puts HMRC manual BIM45700 under FTT scrutiny

Post comment

Categories

- Landlords (19)

- Real Estate (9)

- Renewables & Green Issues (1)

- Rental Property Investment (1)

- Tenants (21)

- Uncategorized (12,592)

Archives

- April 2026 (17)

- March 2026 (72)

- February 2026 (55)

- January 2026 (52)

- December 2025 (62)

- August 2025 (51)

- July 2025 (51)

- June 2025 (49)

- May 2025 (50)

- April 2025 (48)

- March 2025 (54)

- February 2025 (51)

- January 2025 (52)

- December 2024 (55)

- November 2024 (64)

- October 2024 (82)

- September 2024 (69)

- August 2024 (55)

- July 2024 (64)

- June 2024 (54)

- May 2024 (73)

- April 2024 (59)

- March 2024 (49)

- February 2024 (57)

- January 2024 (58)

- December 2023 (56)

- November 2023 (59)

- October 2023 (67)

- September 2023 (136)

- August 2023 (131)

- July 2023 (129)

- June 2023 (128)

- May 2023 (140)

- April 2023 (121)

- March 2023 (168)

- February 2023 (155)

- January 2023 (152)

- December 2022 (136)

- November 2022 (158)

- October 2022 (146)

- September 2022 (148)

- August 2022 (169)

- July 2022 (124)

- June 2022 (124)

- May 2022 (130)

- April 2022 (116)

- March 2022 (155)

- February 2022 (124)

- January 2022 (120)

- December 2021 (117)

- November 2021 (139)

- October 2021 (130)

- September 2021 (138)

- August 2021 (110)

- July 2021 (110)

- June 2021 (60)

- May 2021 (127)

- April 2021 (122)

- March 2021 (156)

- February 2021 (154)

- January 2021 (133)

- December 2020 (126)

- November 2020 (159)

- October 2020 (169)

- September 2020 (181)

- August 2020 (147)

- July 2020 (172)

- June 2020 (158)

- May 2020 (177)

- April 2020 (188)

- March 2020 (234)

- February 2020 (212)

- January 2020 (164)

- December 2019 (107)

- November 2019 (131)

- October 2019 (145)

- September 2019 (123)

- August 2019 (112)

- July 2019 (93)

- June 2019 (82)

- May 2019 (94)

- April 2019 (88)

- March 2019 (78)

- February 2019 (77)

- January 2019 (71)

- December 2018 (37)

- November 2018 (85)

- October 2018 (108)

- September 2018 (110)

- August 2018 (135)

- July 2018 (140)

- June 2018 (118)

- May 2018 (113)

- April 2018 (64)

- March 2018 (96)

- February 2018 (82)

- January 2018 (92)

- December 2017 (62)

- November 2017 (100)

- October 2017 (105)

- September 2017 (97)

- August 2017 (101)

- July 2017 (104)

- June 2017 (155)

- May 2017 (135)

- April 2017 (113)

- March 2017 (138)

- February 2017 (150)

- January 2017 (127)

- December 2016 (90)

- November 2016 (135)

- October 2016 (149)

- September 2016 (135)

- August 2016 (48)

- July 2016 (52)

- June 2016 (54)

- May 2016 (52)

- April 2016 (24)

- October 2014 (8)

- April 2012 (2)

- December 2011 (2)

- November 2011 (10)

- October 2011 (9)

- September 2011 (9)

- August 2011 (3)

Calendar

Recent Posts

- Property118 puts HMRC manual BIM45700 under FTT scrutiny

- House prices dip in March as annual growth also slows

- Nearly 1 in 5 landlords planning to exit the market entirely

- Tenant starts fight with management?

- What the latest Property118 survey results means for mortgage lenders: fewer landlords, different behaviour